Introduction

It has been seven years since the global financial crisis. Interest rates in most developed economies have been reduced to near zero (or negative) and central banks have embarked on significant quantitative easing (QE).

According to theory, central banks control and manage inflation. Why then, during unprecedented global central bank efforts, is inflation still low? Moreover, why does it continue to fall?

Inflation is an important investment cost and opportunity |

As we approach the US Federal Reserve’s most telegraphed interest rate decision in 10 years, investors appear focused on whether the cash rate will increase by 0.25% or not.

At Quay, we are relatively agnostic about the movement in nominal interest rates. (Please refer to Investment Perspectives 6: Listed Property and rising interest rates, for more on this point.)

Interest rates relative to inflation (real interest rates) are far more important to investment returns. Therefore, inflation is just as important a factor to focus on as any central bank decision.

Can central banks actually influence inflation?

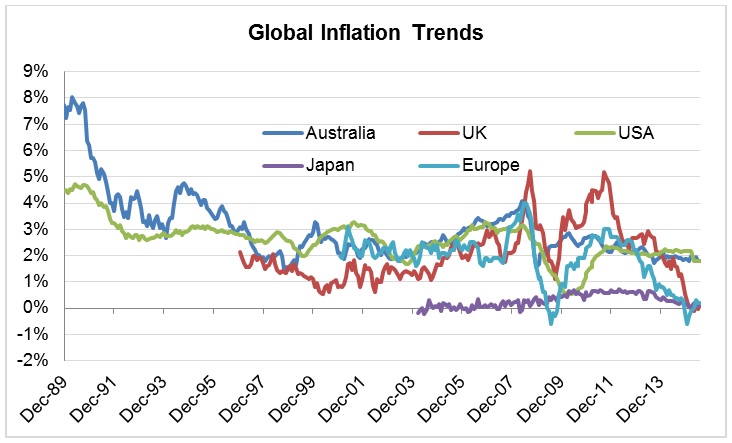

Of course there has been a recent decline in commodity prices (notably oil) and that will have an impact on today’s low inflation data. However, the declining inflation trend has been observed over many years. Over the same timeframe, official interest rates have also been reducing. Should it not be that lower interest rates lift inflation? What happened to the central bank model?

We think there are a number of arguments to suggest central banks act in a manner that is actually causing low inflation – contrary to popular commentary.

Maybe real interest rates normalise, not the nominal rate?

The theoretical construct of nominal interest rates can be summarised as follows:

I(n) = I(R) + P

Where:

I(n) = nominal interest rate

I(R) = real interest rate

P = inflation

Theoretically, long-term nominal interest rates tend toward an equilibrium (demand and supply for money and investment). Therefore, reducing the cash rate is really cutting the short-term real interest rate.

Since the long run cash rate normalises, it requires inflation (P) to rise over time. But what if the opposite were true?

What if real interest rates normalised over time? Then a lower cash rate would result in a lower inflation rate. And since the central bank is always in control of the nominal interest rate, this outcome seems not only plausible, but is supported by the evidence of low global inflation.

While the world awaits the normilisation of interest rates, perhaps it is already happening?

Low interest rates are deflationary

To understand this point, it is important to understand modern banking and how monetary policy works.

Lower interest rates in isolation are a zero sum game. Lower interest expense for households and business are offset (to the dollar) by lower interest income for depositors and savers. This is because bank assets (loans and cash) are equal to liabilities and equity (deposits bonds, etc.).

The real benefit of lower interest rates is to encourage credit creation. The new loan creates the new deposit, which is spent in the real economy; credit growth drives the overall economy.

But what happens during deleveraging in a post financial crisis world? Credit growth becomes anaemic, no matter how low interest rates fall. The credit growth engine stalls. So how is this deflationary?

The fact is most western governments are net interest payers (accumulated deficits). This means the non government sector is a net recipient of interest income. Lower interest rates may be a zero sum game within the private sector, but actually reduces the net interest income to the private sector from the government. The government saves net interest, but at the expense of the private sector. Operationally, the result is no different to taxation.

Quantitative easing is deflationary

Since the Federal Reserve embarked on its QE program in 2008, the economic consensus was for rising inflation due to central bank “money printing’’. But QE has failed to lift inflation. Why? We believe there are two reasons.

Firstly, increasing bank reserves does not encourage credit growth. New credit requires a willing lender and borrower. As the private sector de-leverages, no amount of reserves will encourage the private sector to take on more debt.

Secondly, QE is not money printing at all, but really an asset swap. Central banks acquire long dated monetary assets (like bonds) in return for reserves (or cash from non-bank sellers).

It is akin to moving one’s term deposit account to a savings account. The purchasing power across the wider economy is no differnet as a result of QE. But the operation is deflationary because central banks are removing high yielding monetary assets from the private sector and in return are providing low yielding cash.

Like low interest rates, operationally QE was really no different to a tax on the private sector. Not convinced?

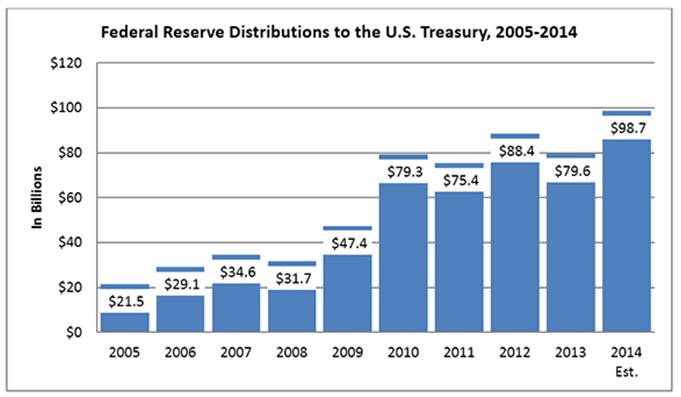

Every year the US Federal Reserve reports an operating surplus and associated ‘dividend’ payable to the US Treasury. The chart below highlights the trend in the annual payments. The increase in payments from 2008/2009 reflect the increase in net interest payments to the Federal Reserve, that would have normally be paid to the private sector.

Concluding thoughts

What happened to inflation?

- Many of the strategies employed by central banks are acting as a mild deflationary force.

- Low interest rates and QE are depriving the non-government sector of net interest income – operationally no different than a tax.

- Rising interest rates with low and falling inflation will lift inflation over the long term – but in the short term, higher real interest rates may disrupt the pricing of financial assets

To be clear, we are not suggesting the inflation demon is gone forever. In fact, if the Federal Reserve begins to increase interest rates this year, it may have positive implication for inflation and the economy in general as net interest income to the private sector increases. In the short term however, volatility in financial markets will likely persist.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.