Gordie Howe International Bridge, joining Detroit to Canada. Source: 4D Infrastructure

A cornerstone of our investment process is company management meetings and site visits. These meetings serve several purposes, including providing an insight into management – how they think and run their business – and whether management priorities align with ours as investors. Our Company Quality Grading process involves explicitly ranking company management, so first-hand contact is vital.

The 4D investable stock universe is dispersed broadly around the globe. This necessitates our team travelling widely to call on companies, meet management and conduct site visits. This invariably provides a great insight into not only the specifics of the company being visited, but also a real perspective on what is happening more broadly in the relevant sector, economy and society. We prepare detailed notes after those meetings which capture and relay the key issues and themes of the day.

This is the sixth in our series of Trip Insights, where we share those experiences. It follows a trip during 2018 when Peter Aquilina, 4D Global Senior Investment Analyst, completed an extensive company engagement and calling program in the United States meeting with management teams from Oil & Gas Infrastructure, Regulated Utilities and Renewables.

Trip Agenda

United States, October 2018

Introduction

With global markets increasingly uncertain due to economic and geopolitical concerns, in recent months US utilities have received increased interest from domestic and global investors. This is probably due to the low cashflow volatility of the sector, and it being largely domestic focused with little earnings exposure to foreign trade or tariffs. This recent strong price performance is unusual for utilities at a time when the US Federal Reserve is increasing the cash rate, which is expected to continue into 2019.

In October 2018 4D travelled to the North East and Mid West of the US to explore the issues supporting and challenging some of the better performing “pure play” regulated utilities in the US.

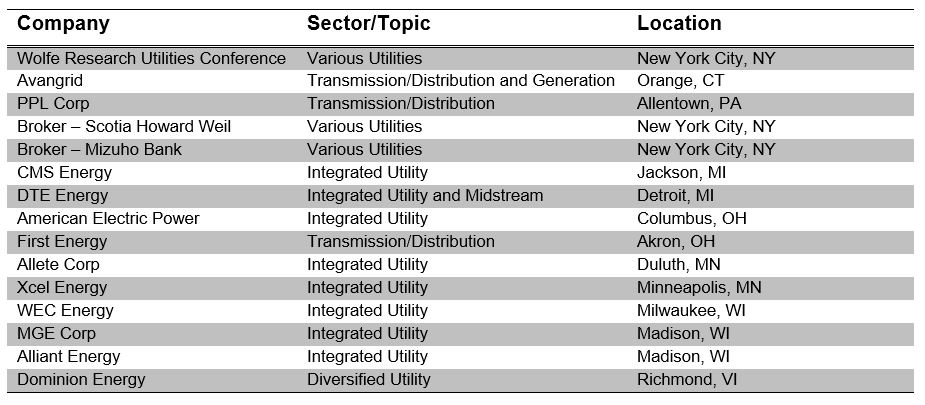

The trip started in New York at the Wolfe Utility conference. A collection of utility management teams presented their respective company’s strategy, growth forecasts and risk/opportunities. Many companies regularly update their growth capex guidance in Q3 and these presentations were a pre-cursor to that. Some of the key themes included:

- multiple investment drivers for growth – execution is dependent upon customer benefit being proven;

- a key focus of customers and regulators is ensuring bills remain affordable – this usually meant keeping bill increases in line with or below inflation;

- operational performance, efficiency and customer satisfaction are the key focus for regulators;

- strengthening of balance sheets continues through equity issuances, and sales of non-core assets;

- concerns about regulatory approvals and execution of “mega” projects such as nuclear facilities, electric and gas transmission connections, and offshore wind; and

- consolidation of utilities continues to be considered, although is becoming more difficult because of high market valuations and less tax benefit from holding company debt following the recent implementation of the Tax Reform and Jobs Act (TRJA).

North East utilities – growth and value opportunities

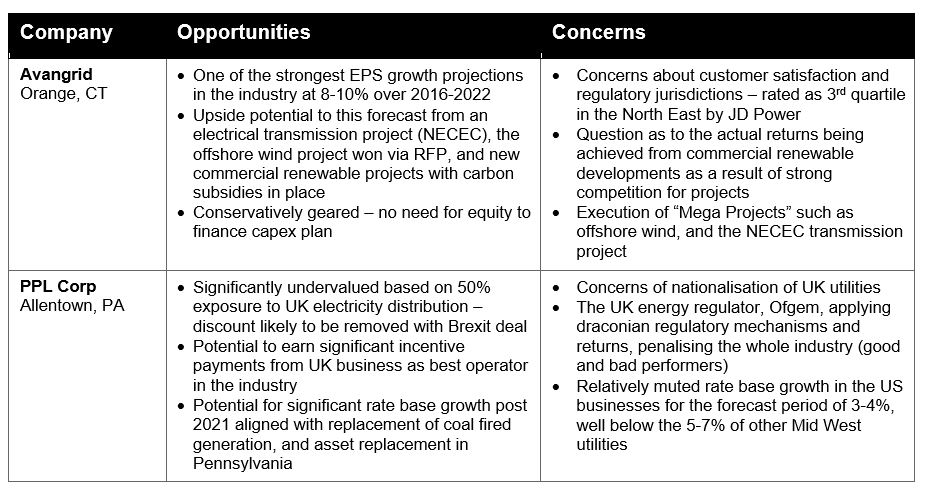

We then visited companies in the North East of the US which operate within the PJM energy market (Pennsylvania New Jersey Maryland Interconnection LLC). Avangrid and PPL Corp have experienced poor share price performance over the past year (-3.5% and -14.5% respectively). The opportunities and challenges facing each of the companies are quite distinct, but both have strong links to Europe.

Avangrid is majority owned by Spanish utility Iberdrola. The company has a very strong growth profile driven by 9% forecast rate base growth in its regulated utility businesses, and significant investment in commercial renewable generation.

PPL Corp’s earnings are split roughly 50/50 between US and UK utilities. The company’s growth is relatively muted over the next five years (particularly in the UK), but it potentially represents a deep value opportunity based on its poor share price performance largely resulting from its exposure to UK regulated utilities, which have been shunned by investors based on nationalisation and regulation concerns.

Michigan utilities – prime performers

We then travelled to the Mid West, starting in the state of Michigan. Hiring a car for the first time in the US, and having booked the smallest option available, we were upgraded to the pictured Chevrolet Camaro at no extra cost. Welcome to Motor City!

For at least the last 10 years the utilities in Michigan, CMS and DTE Energy, have developed a track record as some of the best operational and financial performers in the industry. This has been attributed to:

- a supportive and rational regulatory environment; and

- operational best practice of employees, borrowed from the automotive industry which has traditionally been based in the state.

CMS and DTE Energy have similar characteristics in that they are both strong performers and are favoured by utility investors (indicative in their relative P/E multiple valuations). They both at least achieve their allowed regulatory returns through good regulatory and customer relationships; they both have strong Earnings Per Share (EPS) growth forecasts with midpoints of 6% and 7% respectively for DTE Energy and CMS; and both have long track records (10 years+) of achieving or exceeding guidance earnings.

One key difference between the companies is that DTE Energy’s earnings have a ~25% exposure to unregulated midstream assets, whereas CMS has much smaller unregulated business exposure, via a financing business. DTE’s midstream business developed opportunistically, beginning when the geographically close, gas rich resource basin, the Marcellus/Utica, was discovered in the early 2000s. The company will continue to look for opportunities associated with its existing business that match the risk profile of the utility business – long term contracted assets with high credit counterparties.

The key investment risk facing these utilities is that they both currently trade at high relative P/E multiples compared to the industry, potentially indicating that the strong growth profile is already priced into expectations by shareholders. With the continued increase in rates by the Federal Reserve, these utilities don’t have much in terms of surprising to the upside to offset any negative share price reaction because of increasing rates.

Ohio utilities – making a comeback

Moving to Columbus, Ohio we visited the offices of American Electric Power (AEP). The company recently had its proposed mega project, a 2,000MW wind generation facility called “Wind Catcher”, rejected by the Texas regulatory commission. Obvious questions surrounded the learnings from the failed approval process, and what next? In terms of future strategy, the answer is the company will continue to invest in a number of investment drivers across its electricity distribution, transmission and generation businesses with the goal of delivering 5-7% EPS growth out to 2022.

Travelling two hours to Akron, we then met with the management team of First Energy (FE). One of the key focus areas of FE has been to complete the exit from its merchant generation subsidiary business through the bankruptcy process the subsidiary is engaged in. This process is largely complete, having agreed terms with creditors and the agreement signed off by the bankruptcy court in September 2018. The company is now focused on driving efficiency and operational excellence in its core regulated businesses.

Both these Ohio utilities have dealt with specific issues which have arguably been overhangs on their stock price in the recent past. Looking forward, they both also have a number of attractive investment qualities which include:

- both are pure play regulated utilities;

- geographically diversified operations in largely supportive regulatory jurisdictions (with exceptions);

- strong relative EPS growth forecasts of 5-7% for AEP and 6-8% for FE; and

- strong operational performance and achieving constructive regulatory outcomes with regulators.

Minnesota utilities – delivering renewables

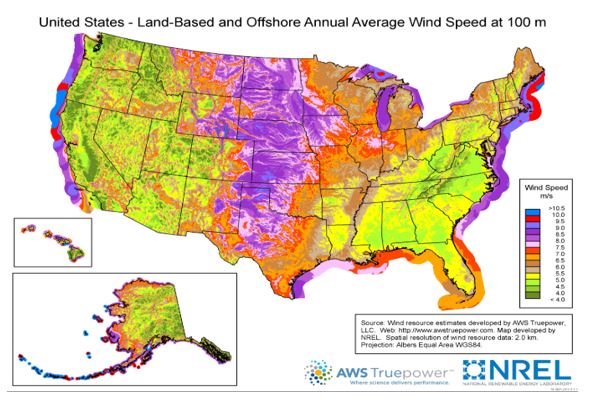

The next state visited after Ohio was Minnesota. Along with its neighbouring states in Wisconsin and the Dakotas, Minnesota has some of the best conditions in the US for renewable wind generation. The combination of unpopulated regions and strong wind resource provides attractive potential land sites for wind generation development projects. New projects with the latest technology can achieve capacity factors in the region of +45%. This map of the US by the National Renewable Energy Laboratory gives an indication of average wind speeds by geography, and therefore the best wind resource areas in the country.

After driving for over two hours from Minneapolis, the capital of Minnesota, to Duluth, near the Canadian border and on the shores of Lake Superior, we met with management of Allete Energy. The company is one of the smallest by market cap in the utility universe, and its regulatory jurisdiction is relatively unpopulated, with key customers being the mining companies that operate in the region.

Allete presents itself as being a steward of environmental sustainability. This is supported by its regulated subsidiary, Minnesota Power, which has set the goal of achieving 44% renewable generation capacity by 2020. Allete also has a renewable wind energy subsidiary that owns a significant amount of unregulated but contacted generation capacity (535MW in operation at time of writing). This renewable business is expected to be one of the key drivers of earnings, with 185MW of additional generation developed in 2019 and an additional 200-400MW before the end of 2022. This translates into annual earnings growth of around mid-double digits.

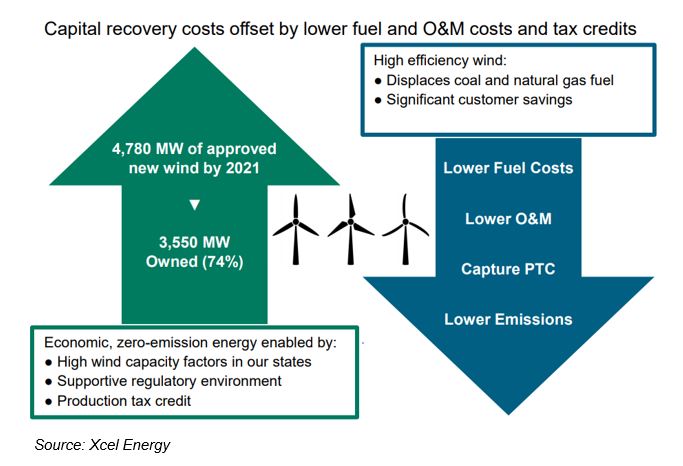

Back in Minneapolis we met with management of Xcel Energy, another large utility that is diversified across multiple geographic jurisdictions. A core piece of its strategy is the “Steel for Fuel” initiative, which looks to deliver cost savings for customers through the transition from conventional fossil fuel generation to wind generation. This is shown in the following slide from their investor presentation.

Xcel understands that one of the keys to executing on this strategy is to achieve regulatory support for the investment, which is driven by customer satisfaction with service levels and bills. Xcel has communicated the objectives of achieving top quartile customer satisfaction through enhanced security, reliability and automation; and keeping operating and maintenance costs flat at 2013 levels ($2.3 billion) through to 2022, therefore reducing customer bills.

Wisconsin utilities – premier operators

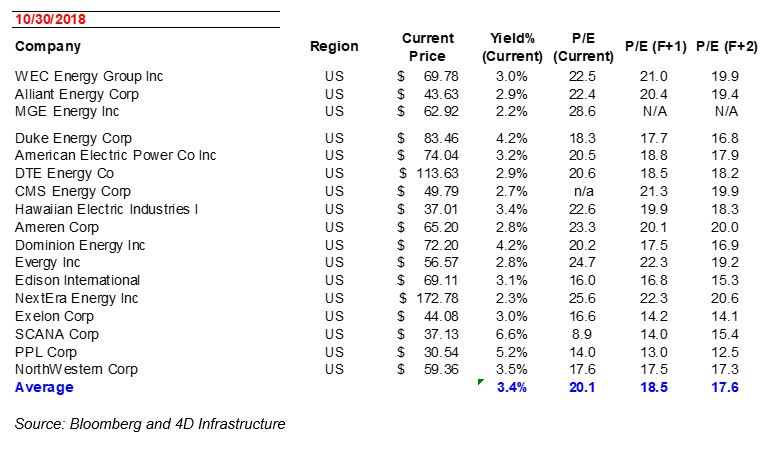

Next stop was a short flight to the neighbouring state of Wisconsin, where we visited companies in the cities of Milwaukee and Madison. Wisconsin is considered by analysts to be among the most supportive regulatory environments in the US. UBS has ranked it as a Tier 1 jurisdiction (of five Tiers, with one being most attractive) in its North American Regulatory Jurisdiction Rankings. The utilities in the state have some of the strongest forecast earnings growth rates and have demonstrated predictable earnings over an extended period. They have been favoured by investors, based on their P/E valuation multiple premiums compared to peer utilities in the US.

The three companies at the top are based in Wisconsin and have P/E multiples in excess of two turns higher than the average of their peers. Many factors play into valuation multiples, but it is probably not a coincidence that all Wisconsin utilities have a valuation premium compared to peers on a multiple of earnings basis (P/E).

Our first meeting was with WEC Energy at its headquarters in Milwaukee, which was built in 1905.

WEC is one of the best financial performers in the industry. The company has delivered an average annual return of 15% since 2002 and exceeded its annual EPS guidance every year since 2004. WEC has delivered this through:

- developing strong relationships with the regulators in its jurisdictions;

- delivering operational excellence through strong reliability;

- maintaining bills for customers;

- investing well in its regulatory companies; and

- beginning the transition from coal generation to wind and gas fuelled.

Looking forward, management suggested that there were a number of investment drivers available to the company across regulatory jurisdictions to continue to deliver growth in the long term.

The company recently announced significant changes to its management team, including new President Kevin Fletcher. A number of questions at the meeting revolved around the ability of Mr Fletcher and new members of the management team to continue to deliver the operational and financial excellence that has made WEC such a favoured company by investors. Management expressed that operational excellence and the desire for continuous improvement is ingrained in the culture of the company. This, combined with Mr Fletcher’s strong operational background, should put the company in good stead to continue delivering operational and financial performance in the future.

We subsequently travelled to Madison, Wisconsin which has a relatively well educated, high socio-economic demographic, plus the University of Wisconsin is based in the city. As a result, the city has a relatively low unemployment rate (~3.3%) and strong economic growth driven by high tech industries including health and bio-tech.

This well-educated customer base has demonstrated a preference for renewable energy and customer choice initiatives, which provides additional investment drivers for utilities in this jurisdiction. An example of this is the pictured Blount Generation Station, situated in the centre of Madison, which was converted from coal to gas fuelled in 2011.

In Madison we met with the smaller, regionally based utilities MGE Energy and Alliant Energy, with operations in Wisconsin and Iowa. Both these companies:

- are pure play regulated utilities;

- have strong relationships with the Public Service Commission of Wisconsin and other regulatory bodies they liaise with;

- have a number of investment drivers, some unique as a result of their demographic;

- are very focused on Environmental, Social and Governance issues; and

- take a conservative approach to providing market guidance on forecasted capital expenditures and therefore earnings growth.

Virginia utilities – last stop

To finish the trip, we passed through the city of Richmond in the state of Virginia. This is the headquarters of Dominion Energy. Unlike the pure play regulated utilities visited in the Mid West, Dominion is a diversified utility with a core regulated utility business and a number of ancillary investments in midstream gas – transport pipelines and gathering and processing networks, a Liquified Natural Gas (LNG) facility, and merchant generation (some with long term contracts in place). The core regulated utility, Virginia Energy and Power Company (VEPCO), has strong regulatory relationships in the state, with a number of investment drivers and a strong regulatory return earned on investment.

Earlier in 2018, Dominion was experiencing some financing concerns which provided an overhang on the stock performance. The concerns were driven by excessive parent company debt, the negative cashflow impact on utilities from tax reform legislation, and because its key funding vehicle, the Master Limited Partnership (MLP) in Dominion Energy Partners (DEP), had fallen out of favour with investors in line with other MLPs in the market. Dominion communicated a financing strategy which involved a number of steps including a forward equity issuance, the sale of non-core assets, and raising of a project finance bank facility at its LNG project, all with the intention of repaying holding company debt. These have largely now been completed, leaving the company in a stronger credit position.

The company is looking to continue to potentially branch into other forms of non-regulated business, with suggestions it may look to enter the offshore wind generation market, with projects planned off the east coast of the US including Virginia. This suggests the company has not lost its appetite to undertake further complementary investments, even outside the regulatory business.

Dominion is also active from an M&A perspective, having submitted a stock for stock merger proposal for the utility based close by in South Carolina, SCANA Corp, in January 2018. The merger required approval from the South Carolina Corporation Commission (SCC), and if successful the transaction would increase the proportional contribution of regulatory utilities to total earnings of the merged entity (the merger was subsequently approved by the SCC in December 2018).

Download a copy of the article here.