Myths still persist

“You’re mad.”

This was not an uncommon response from some friends and family when I told them in December 2013 I was leaving a relatively safe job at Credit Suisse to start a global real estate strategy. Not because they believed starting a new business was risky (it is), but because of the perception that interest rates were expected to rise (QE was ending) and it was common knowledge that real estate will perform poorly in such an environment.

“People will no longer search for yield, but growth,” I was told.

Five years later, the Fund has returned 15.4% p.a., not only outperforming our CPI + 5% objective, but also exceeding the so-called ‘growth option’ of local and global equities.1

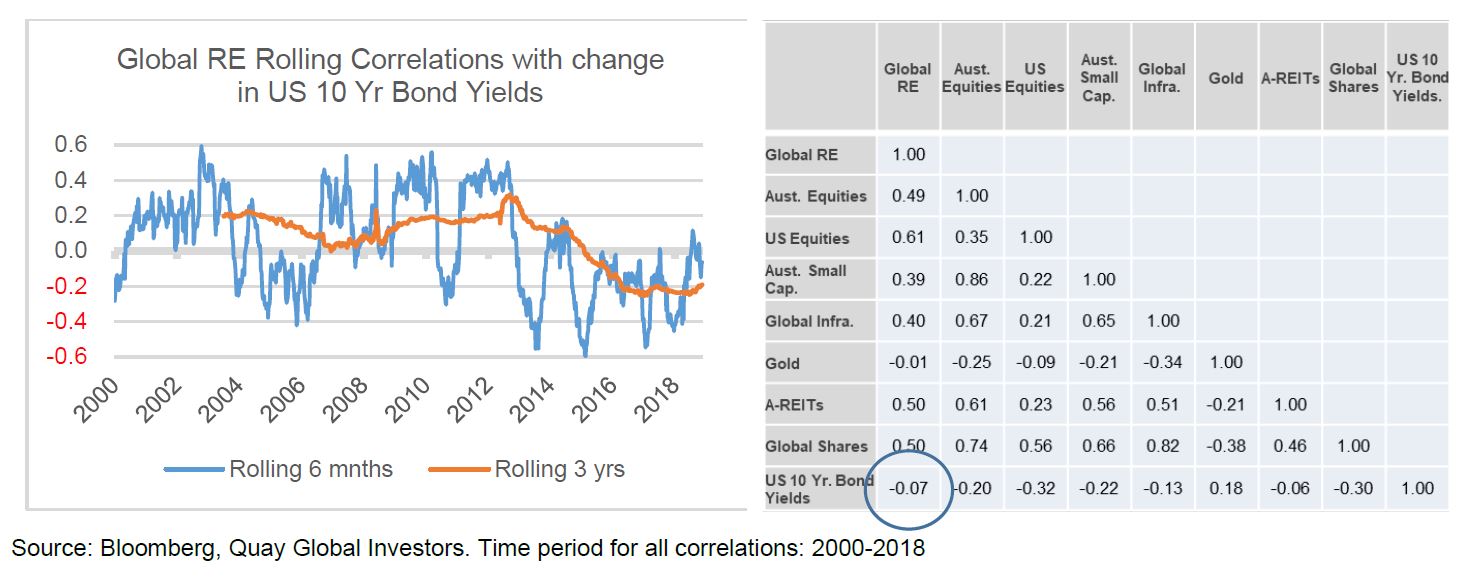

We have long argued real estate can be sensitive to interest rates (especially change in bond yields) in the short term, but the correlation is rarely static. The relationship was predominantly positive between 2004 and 2014 – global real estate prices rose at the same time bond yields were increasing (see below) and over the longer term the correlation between interest rates and unhedged global real estate is zero. That is, for long term real estate investors, rising interest rates are the least of your concerns.

Even today, we sometimes get pushback on this idea. Of course, this is understandable because the recent rally in global bond yields coincided with the rally in listed real estate.

But even more recent data dispels the myth of real estate and interest rates. For example, in August 2016, US bond yields reached an all-time low of 1.35%. If we had told investors that three years later US bond yields would be +2% (reflecting a substantial 50% increase in yield) and after peaking at 3.2%, most would argue this would be a headwind for total returns for the sector.

However, over the past three years our US stocks have returned +33.8%.

What keeps us awake at night? It’s never interest rates. If there are any macroeconomic headwinds for real estate returns, it’s excess supply and the general economy. And rising interest rates are usually a sign of a pretty good economy.

Nevertheless, the interest rates myth persists.

A good theory can lead to good outcomes – part 1

Our initial premise was that investing in real estate shouldn’t be about beating some arbitrary index, but rather finding the best listed real estate opportunities with a focus on delivering sustainable real (after inflation) total returns.

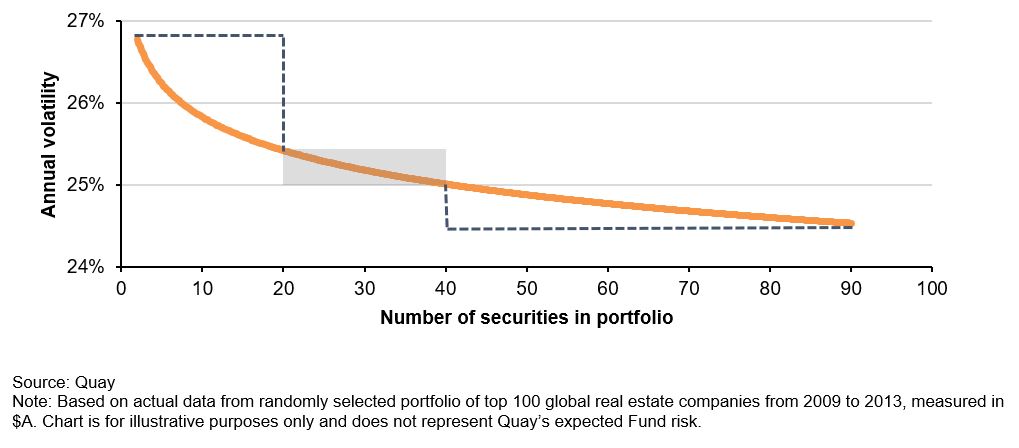

The global real estate opportunity set is large, and at any one time there can be a vast array of attractive investment opportunities. Therefore, one of the questions we needed to address prior to launching the fund was: what is the appropriate number of securities to hold to deliver relatively low volatility, without overly diluting our best investment ideas?

We approached this problem by running Monte Carlo simulations of random unhedged global real estate portfolios ranging from two securities up to 90 securities over the period from 2009 to 2013. We plotted the volatility of each simulation, through which we ran a line of best fit as depicted by the following chart[2].

Average annual standard deviation of random global real estate portfolios by number of securities

It was clear from our analysis that most of the portfolio diversification benefits of additional securities occurred with the first 20 stocks – and beyond 40 stocks, the benefits were minimal.

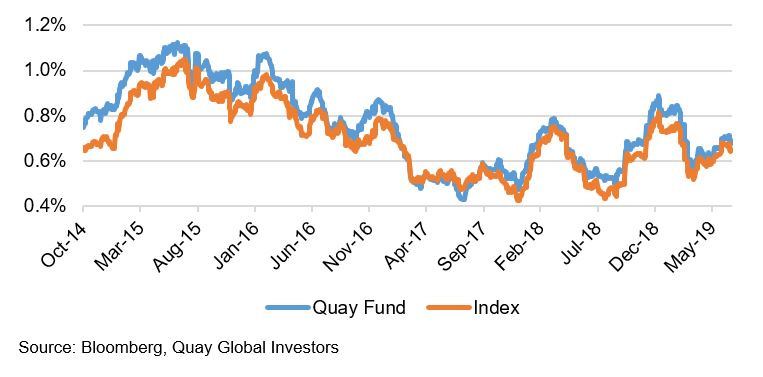

Since its launch in July 2014, the Quay Global Real Estate Fund has owned between 21 and 27 investees, with an average holding number of 24. So how did we do?

Rolling three-month volatility

As the chart above highlights, the Fund’s 21-27 stock portfolio rolling volatility is not significantly higher than the global real estate index with +310 constituents. This means our portfolio can generate returns from the best ideas without significant volatility. After five years of track record, we continue to believe our approach (supported by our early research) provides a sensible risk-return trade-off for our investors.

A good theory can lead to good outcomes – part 2

To currency hedge or unhedged?

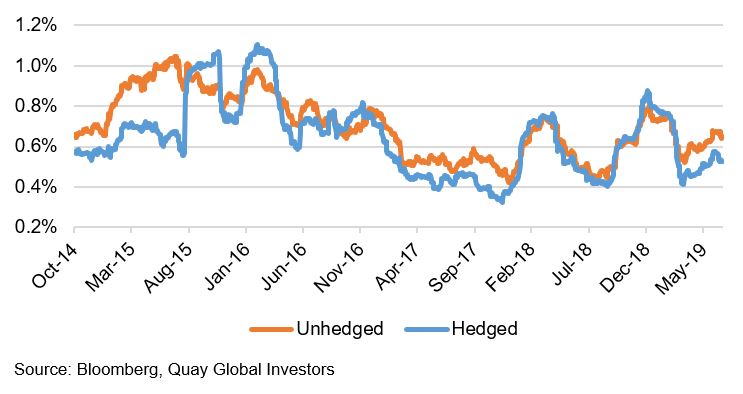

When we contemplated launching the Fund, we observed almost all the existing global real estate strategies were currency hedged. Interestingly, almost no global equities strategies were hedged.

As we thought about our strategy, everything began with a blank piece of paper – we were prepared to design the strategy by challenging the norms. And our research found that for an Australian dollar fund, an unhedged strategy was a lower risk proposition for our investors[3]. Why?

- In periods of market stress, the $A generally depreciates (while USD and Yen appreciate), offsetting near term losses that may occur with our individual securities.

- While we argue interest rate movements have no impact on long term real estate performance, they do in the short term. They can also impact currencies in the short term, but in the opposite direction – again providing a buffer for $A returns.

- Hedging can precipitate liquidity issues, especially during times of economic and market stress (the worst time for liquidity issues). Remaining unhedged means we can be patient during such times, and never be forced to sell / liquidate positions at distressed prices to meet a margin call.

The following chart highlights that the rolling volatility of the global real estate hedged index is generally lower than the unhedged index, except in times of heightened market risk when the unhedged index benefits from the offsetting $A movements. Again, after five years we continue to believe an unhedged strategy will result in lower volatility and is less risky during times of market disruption – and, most importantly, avoid costly liquidity events.

Rolling three-month volatility of index

Being overly conservative is just as costly as being overly optimistic

The cornerstone to our strategy is capital preservation. Of course, as a ‘long only’ strategy we cannot deliver on this promise over a short period of time due to market volatility and cycles, but we expect to do so over the medium to long term.

With this mindset, it’s normal to underwrite each investment we make with a level of conservatism. It’s natural to have a ‘margin of error’ when modelling the underlying cashflows of prospective or current investees.

But while being conservative may give us comfort, it can also lead to missed opportunities.

One of the errors we have made in the past five years was to sell too early. In this case it was Link REIT (Hong Kong retail). We acquired the stock for ~HK$40 / share, and sold in the low HK$50s. It was a good turn, but as the company earned ~HK$2/share, we felt it was hard to see our CPI + 5% total return above $50. Sure, the company had a terrific asset enhancement program, generating substantial returns on capital, but how long can that last? Meetings with management never gave us too much comfort that the programs would last far beyond their disclosed pipeline – so we ‘conservatively’ assumed they would last 2-3 more years and then normalise. On this basis a +HK$50 share price was challenging from a valuation perspective. So, we liquidated our position.

Today Link REIT is HK$95/share, and the substantial asset enhancement programs remain ongoing.

Ouch.

The lesson? It’s okay to be conservative, but we need to remain mindful of ensuring we’re not leaving returns on the table. This lesson has served us well in recent years, as some of our ‘winners’ continue to deliver.

A (relatively) small local team is a huge advantage

We have an investment team of four individuals – all located in Sydney.

In some presentations we are asked how a team of four located in Sydney can effectively run a global real estate strategy. Sometimes I feel like our response should be, “How can a disparate team of individuals scattered across multiple time zones run any strategy?”

We always believed the size and location of our team is an advantage. Over time, our belief in this idea has only increased.

The biggest advantage is being away from the day-to-day noise that may distract us from our investment goals – identifying attractive real estate investees with long secular runways, sensibly financed, acquired at a sensible price.

I quite often wonder if we had teams in other countries whether we could ignore such noise – and whether having a larger team would compel us to own more securities as each voice ‘on the ground’ is perceived to be too much of an information advantage to ignore. I feel a larger geographically diverse team would only lead to us owning more securities and increasing our turnover.

Instead, we remain disciplined in the number of securities we own (26 today) and our turnover remains low (15% per annum since inception and 10% over the past 12 months). To be clear, we don’t target low turnover – and we never promise it will always be low – but it should be a long-term outcome if we are truly aiming to allocate capital to sectors with long secular tailwinds.

Most fund managers like to quote their favorite investment hero or guru. So, let me indulge with one here:

“If investing is entertaining, if you're having fun, you're probably not making any money. Good investing is boring.” – George Soros

Our relatively small team of people, all located in Sydney, are insulated from the excitement of the daily noise and allowed to focus on long term returns, while keeping the entire process as boring and predictable as possible.

Concluding thoughts

Much is written regarding the benefit of compounding returns in the world of investment. The maths behind this concept is pretty clear.

Less discussed, but equally important, is the compounding effect of knowledge. The ability to learn from mistakes and adjust and enhance your approach accordingly is just as valuable in the world of investment. If we learn from our own mistakes and better understand our wins, then we should be better investors today than when we began five years ago. And we fundamentally believe this to be the case.

Download a copy of the article here.

[1] For details, refer to Investment Perspectives: Why does real estate outperform equities?

[2] For more on this analysis, refer to Investment Perspectives: The building blocks of a portfolio.

[3] For a more detailed analysis, refer to Investment Perspectives: hedged or unhedged?