Source: Calgary Airport; 4D Infrastructure

A cornerstone of our investment process is company management meetings and site visits. These meetings serve several purposes, including providing an insight into management – how they think and run their business – and whether management priorities align with ours as investors. Our Company Quality Grading process involves explicitly ranking company management, so first-hand contact is vital.

The 4D investable stock universe is dispersed broadly around the globe. This necessitates our team travelling widely to call on companies, meet management and conduct site visits. This invariably provides a great insight into not only the specifics of the company being visited, but also a real perspective on what is happening more broadly in the relevant sector, economy and society. We prepare detailed notes after those meetings which capture and relay the key issues and themes of the day.

This is the seventh in our series of Trip Insights, where we share those experiences. It follows a trip in 2019 when Mark Jones, Senior Investment Analyst, completed an extensive company engagement and calling program in Canada, meeting with management teams from Oil & Gas Infrastructure, Regulated Utilities, Renewables and Transport (road, rail, air and sea).

Trip Agenda

Investor meetings included the following companies / regulators:

|

Company |

Sector/Topic |

Location |

|

Enbridge |

Oil & Gas Storage / Transportation |

Calgary |

|

Gibson Energy |

Oil & Gas Storage / Transportation |

Calgary |

|

Inter Pipeline |

Oil & Gas Storage / Transportation |

Calgary |

|

Keyera |

Oil & Gas Storage / Transportation |

Calgary |

|

Pembina Pipeline |

Oil & Gas Storage / Transportation |

Calgary |

|

Tidewater Midstream |

Oil & Gas Storage / Transportation |

Calgary |

|

TransCanada |

Oil & Gas Storage / Transportation |

Calgary |

|

Wolf Midstream |

Oil & Gas Storage / Transportation |

Calgary |

|

DP World |

Ports |

Vancouver |

|

Westshore Terminals |

Ports |

Vancouver |

|

Boralex |

Renewables |

Montreal |

|

Northland |

Renewables |

Toronto |

|

Polaris Infrastructure |

Renewables |

Toronto |

|

Alta Gas |

Integrated Regulated |

Calgary |

|

Hydro One |

Transmission & Distribution |

Toronto |

|

Canadian Pacific |

Rail |

Vancouver |

|

Canadian National |

Rail |

Montreal |

|

Canadian Transport Agency |

Rail |

Vancouver |

Overview

Canada is a fertile investment ground for global listed infrastructure (GLI) companies, accounting for approximately 10% of the 4D investment universe by market capitalisation. It is represented by both user-pay assets – most notably rail, oil & gas transportation and ports – and more defensive sectors such as utilities and renewables. Canadian infrastructure companies have also been successful in expanding into other markets, most notably into the US and Mexico (due to geography) and parts of Europe, typically France (due to language).

A review of Canadian GLI stocks encompasses much more than just local investment themes. Significantly, Canada and the US are enjoying an energy renaissance at present with record exports of oil and gas. However, in the case of Canada, the optimal infrastructure solution for that export boom, being new pipelines, has been repeatedly delayed due to political interference. As a result, rail/storage has been playing an increasing role in the transportation of oil and gas.

In this paper we look at the challenge and opportunity for infrastructure (e.g. rail, pipeline and ports) in Canada – how they are capitalising on a once-in-a-generation oil and gas production boom and the impact political risk can have on investment outcomes. High level investment meetings suggest a bias in proposed portfolio positioning to natural gas and NGL infrastructure over oil.

We also look at the:

- Long run potential of decarbonisation / renewables: and the criteria for picking ‘winners’ in a crowded space with investment meetings leading to a preference for renewables in France over other jurisdictions such as the US and Canada; and the

- Comparative advantage of integrating rail and port projects and how Canada has very effectively achieved this.

Canadian oil & gas exports need for infrastructure

In 2018, the US continued its energy renaissance to become the world’s largest producer of crude oil, with production rising to 11 million barrels per day (up from 9.4 million barrels per day in 2017), eclipsing its previous production high reached in 1970. Combined with Canada, which produced 4.6 million barrels per day (up from 4.2 million barrels per day in 2017), the US and Canada make up almost 20% of global oil production, with both continuing to grow as evidenced by year-on-year growth rates.

The majority of the growth in new oil production has been from shale oil, which through hydraulic fracking can release both oil and dry or wet gas. Hydraulic fracturing involves injecting water, sand and chemicals under high pressure into a bedrock formation via the well. Wet gas will include a number of natural gas liquids (NGLs), most notably propane and ethane. Combined production increases in oil, gas and NGLs is a significant demand driver for new infrastructure, leading to a need for:

- gas processing and / or fractionation facilities;

- pipelines and / or rail;

- storage tanks; and

- export terminals.

All of the above share common characteristics of infrastructure assets, namely:

- one-to-many relationships whereby high capital costs are recovered across many counterparties;

- once established, there are significant barriers to entry for replication and / or competition; and

- pricing stability, either through contracts or regulation.

There is a virtuous cycle between oil and gas production and infrastructure. By definition, the higher the utilisation of shared infrastructure, the lower the unit cost should be for oil and gas producers. This makes US and Canada oil and gas more competitive, both locally and increasingly in the global market.

It is the ability to export to global markets that differentiates the US and Canada and, perversely, provides the most interesting investment opportunity, with Canada currently disadvantaged relative to the US. Like the US, Canada now produces oil, gas and NGLs well in excess of local demand – but unlike the US, due to inadequate infrastructure Canada has limited access to global markets, leading to oil and gas producers receiving lower prices.

This is both a challenge and an opportunity for Canadian infrastructure companies, and on this trip was increasingly the focus of investor meetings. Today, Canada mainly exports oil, gas and NGLs to the US through pipelines.

Challenge of oil transport and pipelines

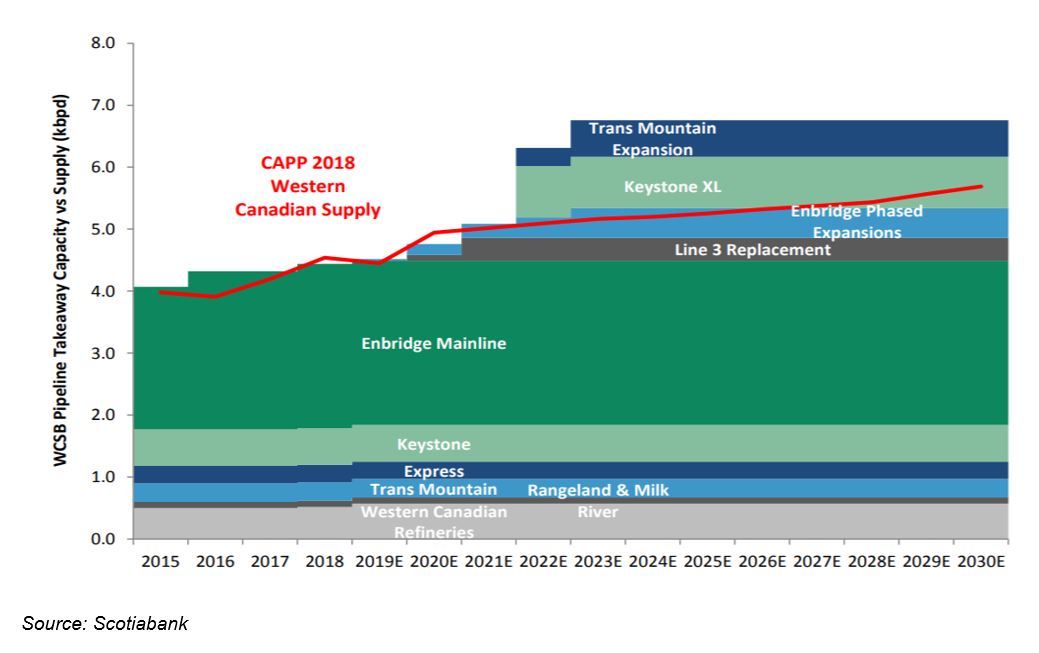

Canadian oil, as can be seen below, is mainly exported through three pipelines (not expected to change). These three pipelines are Mainline / Line 3, Keystone and Trans Mountain. Expansions to these three pipelines have all faced significant delays, causing oversupply – which will only worsen over time as production continues to grow.

Twelve months ago all three pipelines were held by listed infrastructure companies, with Trans Mountain subsequently being nationalised by the Canadian government in response to a lack of confidence in its owners’ (Kinder Morgan) ability to receive political and legal support, and to successfully build it.

Indeed, this is the problem faced by all the major oil pipelines, with Enbridge’s Mainline / Line 3 and Keystone XL being delayed not due to economics, but rather political and legal resistance both in Canada and the US. As Enbridge management highlighted in one of our meetings: ‘it is challenging being in the pipeline business at the best of times’.

Enbridge’s Mainline / Line 3 was the most likely to be built, having reached FID ahead of both Trans Mountain and Keystone XL, but has been stalled due to delays in permitting from the Minnesota government, and then further delayed through the courts. A successful challenge to its Environment Impact Statement led to a revision, such that it may not be built until 2022. This is in contrast to Enbridge’s initial estimate of having it built late 2017 (+5 years post initial estimate)!

On an economic basis, pipelines deliver the lowest cost and safest transport of oil, implying any other mode of transport will be less economic and reduce the competitiveness of Canadian oil. Inadequate pipeline capacity therefore creates perverse winners, with alternative transport modes – in particular rail – benefiting in the short-run, and arguably remains how to position for this ‘market failure’.

Opportunity for rail

Canada’s freight rail network is arguably one of the best in the world, nearly unrivalled in breadth and scale apart from the US. It is defined as infrastructure because of the barriers to entry, pricing power, and it being an essential need for parts of the Canadian economy (e.g. commodities such as grain). Crude oil can be transported by rail (termed ‘crude by rail’), albeit at a higher cost (roughly double) than if transported in pipelines. The challenge with crude by rail is being able to receive an adequate return on capital. Duration of contract tends to be short, with volumes being transported only while pipeline capacity is not available. This makes crude by rail both highly accretive for rail companies, but also risky due to volume risk and stranding of locomotive and rolling stock assets. Acknowledging this, Canadian rail companies have enforced ‘take-or- pay’ contracts with all crude by rail volumes. Take-or-pay contracts allow for a minimum return on capital regardless of whether actual volumes are transported or not.

Reflecting pipeline constraints, Canadian crude by rail peaked in December 2018 when it transported over 350 thousand barrels of crude per day. It is likely this will be surpassed, with potential for a multi-year boom in crude by rail haulage. Crude by rail is highly earnings accretive for rail companies because hauls are generally long, typically from Alberta, Canada to the Gulf Coast, Texas (~4,000 kilometres). This is further reinforced by government intervention to solve this market failure. In December 2018, the Alberta government signed contracts to haul a minimum of 120 thousand barrels of oil per day over three years starting July 2019. To this end, crude by rail could export above 500 thousand barrels of oil per day in the next 6-18 months.

The other ancillary winner is oil storage through tanks or terminal assets. Oil storage tanks are highly contracted assets, typically under long-term fixed fee arrangements with growth predicated on new oil production. Demand for oil storage tanks also increases when flexibility is required on transport.

Flexibility is required when an oil producer batches its oil to a number of different end points via a number of different modes. Today, this is the case for a Canadian oil producer whereby they will batch oil to be transported on a number of pipelines as well as crude by rail. Therefore, oil storage with adjacent connections to pipelines and a crude by rail loading facility has increasing strategic value, as evidenced by growth in oil storage tanks at hubs in Hardisty, Alberta.

A crude by rail loading terminal allows access to many destinations throughout Canada and the US. Rail shipping costs from Hardisty to Cushing, Oklahoma or the Gulf Coast, Texas are not made public, but are estimated by reporting services at between US$12 and US$15 per barrel, with additional terminal fees at both ends. The value of crude by rail was recently highlighted by Imperial Oil, with management commenting ‘rail is increasingly competitive compared to the pipeline alternative, and is an attractive means for us to get to the mid-Western or Gulf coast markets’.

To conclude, in regard to oil transport infrastructure, in the short-run rail and storage will be beneficiaries. In the medium to long-run, we reiterate our view that all three pipelines will go ahead because:

- they are essential services required by the Canadian oil sands industry to remain competitive;

- the Federal Governments in both Canada and the US have reiterated their support for all projects; and

- the companies involved have credible environmental, social and corporate governance track records and reputation.

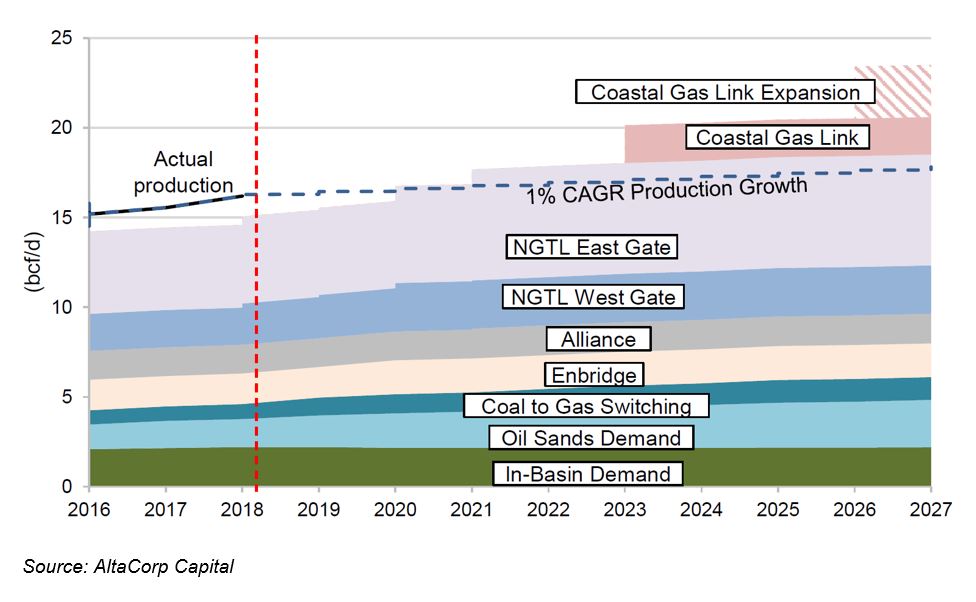

Natural gas and NGLs better placed

In regard to natural gas and NGLs, similar issues prevail. Just like oil, Canada’s production in natural gas continues to grow strongly as TransCanada management highlighted: ‘There is a lot of gas out there just waiting on price’. TransCanada transports over 50% of Canada’s gas production through its Nova gas transmission (NGTL) pipeline system and is the owner of the future pipeline Coastal Gas Link. Because of the oversupply (relative to Canadian local demand), Canadian natural gas tends to trade at a C$1 to C$2 discount to Henry Hub gas prices in the US. Henry Hub is a natural gas pipeline located in Louisiana that serves as the official delivery location for futures contracts on the New York Mercantile Exchange (NYMEX).

Natural gas export is constrained by pipeline capacity, with production more or less matching pipeline capacity. This has been compounded by a lack of liquefied natural gas (LNG) export terminals. By comparison, over the last decade the US has reached commercial operation on a number of LNG export facilities including Cameron, Corpus Christi, Freeport and Sabine Pass, with a large number of additional facilities still to be developed.

Fortunately, Canadian infrastructure companies appear to be much more successful in ‘solving’ for oversupply in natural gas, with both additional pipeline capacity and LNG export facilities in development. This has been due to:

- less political and legal resistance to natural gas and NGL infrastructure;

- taking advantage of Canada’s west coast proximity to Asia relative to Texas, US; and

- creating new markets (for natural gas and NGLs) by going up the value chain.

All of this is leading to Canada’s infrastructure companies successfully deploying significant amounts of investment, which in turn will lead to solid earnings growth over the short to medium run.

To illustrate capital being employed to natural gas pipelines, TransCanada has reached FID (Final Investment Decision) and is building Coastal Gas Link – a 670km pipeline connecting gas from the Montney and Duvernay shale gas basins to the port, with an estimated capital cost of C$6.2bn and an in-service date of 2023. This will be the feeder pipeline for Shell’s LNG Canada, which will allow Canadian gas producers to receive Asia netback natural gas prices (at a significant premium to Canadian natural gas prices). Further, there is a high probability the pipeline will be expanded to allow for incremental trains / supply out of LNG Canada.

In NGLs, a similar dynamic is playing out with Canadian infrastructure companies building export terminals for propane and butane, namely Alta Gas and Pembina Pipeline. Combined with new petrochemical facilities in Alberta, whereby propane will be used as feedstock for higher value products such as propylene and polypropylene, the current oversupply is quickly being addressed. With Canadian infrastructure companies better ‘solving’ for oversupply in natural gas and NGLs, this leads to other opportunities – namely increased production in gas and NGLs, which in turns leads to demand for gas processing / fractionation and storage.

In conclusion, this leads to a bias in portfolio positioning towards natural gas and NGLs infrastructure over oil.

Decarbonisation and picking winners in renewables

Compared to most OECD countries, Canada has a high share of renewables in the energy mix with approximately 17% of Canada’s primary energy coming from renewables (almost double the OECD average). This has allowed a number of local listed infrastructure companies to specialise in renewables, including Boralex, Innergex, Northland Power and Polaris Infrastructure. These companies have invested in Canada – but also in other jurisdictions including the US, Europe and Latin America – across all renewable technologies including wind (offshore and onshore), solar, battery, hydro and geothermal power.

From an investment perspective there is significant structural support for investing in renewables, with the majority of the OECD slowly decarbonising with variable incentives from federal and local governments. IHS Markit forecast approximately 140GW of renewables build in Europe by 2021 and 75GW in the US. There are, however, challenges to be mitigated, including:

- change in contract terms with power purchase agreements (PPA) becoming shorter in duration, with lower or no feed in tariffs;

- jurisdictional diversity intra Europe and between Europe and the US; and

- high levels of competition from incumbent energy players looking to reposition and unlisted infrastructure.

A PPA is a contract between an electricity generator (provider) and a power purchaser (buyer, typically a utility or large power buyer/trader). Due to capital impost associated with energy infrastructure investment and provision, historically typical PPAs have been long duration (>20 years), with pricing indexed to inflation.

In meeting with Canadian renewable companies, each has taken a slightly different strategic approach, leveraging the expertise acquired in the local Canadian market to deploy renewables in other markets. ‘Winners’ by definition will be renewable companies operating in favourable jurisdictions with relatively low competition; and able to achieve relative strong power PPAs. This is achieved by having long-dated / incumbent locally based disciplined management teams with access to flexible capital. Understanding a particular jurisdiction requires time and a learning curve, hence the bias to incumbency.

One particular jurisdiction which appears relatively favourable is France, whereby Canadian companies have a comparative advantage through incumbency and language. France has a target of producing 23% of its total energy needs from renewable energy by 2020, increasing to 32% by 2030. Due to environmental considerations it is very difficult to progress new projects, but when a PPA is signed they tend to be long dated and with an accretive return on invested capital. This is being reflected by new players increasingly moving into the market (e.g. EnBW acquiring VALECO), which further increases the value of incumbents such as Boralex and Innergex.

Integration of rail and port

As highlighted in the discussion on crude by rail, Canada’s freight rail network, provided by a duopoly of Canadian National and Canadian Pacific, is large and fully integrated into most of Canada’s ports. The ‘gold standard’ of this integration is the Prince Rupert container port, which is based on the west coast and can only be accessed by rail. Due to the efficiency of rail versus truck, the Prince Rupert container port (and other Canadian ports such as Vancouver) have grown aggressively, capturing market share from other more inefficient US west coast ports. Owned by DP World, Prince Rupert has grown from 300 thousand containers per year in 2010 to over one million containers per year in 2019. This has driven investment to increase capacity to over two million containers per year by 2025.

A similar story is evident in DP World’s Centerm facility, located on the south shore of Vancouver’s inner harbour. It has the shipside capability for two container berths and moves approximately 60% of its containers by rail. DP World highlighted on tour that it expects to increase container capacity to 1.5 million containers by 2021, relative to a current run rate of 900 hundred thousand containers through the facility annually. The growth in containers in Canada’s west coast ports has in turn led to a boost for Canadian rail providers, with intermodal growth being significant over the last five years. As an example of this, Canadian National’s intermodal volumes have grown at a 5-year CAGR +7% compared to Canada’s GDP at +1.8%. Investor meetings and a rail tour of the Port of Vancouver highlighted that this comparative advantage is continually being refined. Both Canadian National and Canadian Pacific had a number of initiatives to increase capacity in and out of the port, including adding additional sidings to the rail network and coordinating with Vancouver port officials on bridge and tunnel access (north-to-south rail access provided by a single cantilevering bridge). This is facilitated by a joint investment from the Canadian federal government to the tune of C$167m.

This reinforces the quality of Canadian rail companies and the structural long run advantage rail has over road in Canada.

Download a copy of the article here.