We called the decline in property prices back in May 2017. Soon after, prices began to decline, and are now close to 15% below peak in Sydney. The question is: in the current environment, are the worst of the falls behind us?

Quay’s real estate valuation framework

At Quay, we view residential assets as commodity property. When thinking about commodity property, it is important to understand replacement cost. When prices are above replacement cost, a profit motive exists to supply the market with new stock. Conversely, when prices are below replacement, supply is constrained and remains so until prices recover. As a result, prices tend to oscillate around replacement cost, which in turn generally increases in line with inflation.

The gap between house prices and replacement cost is large, but narrowing

So where are we now in terms of this cycle? We can deduce this by looking at the below charts.

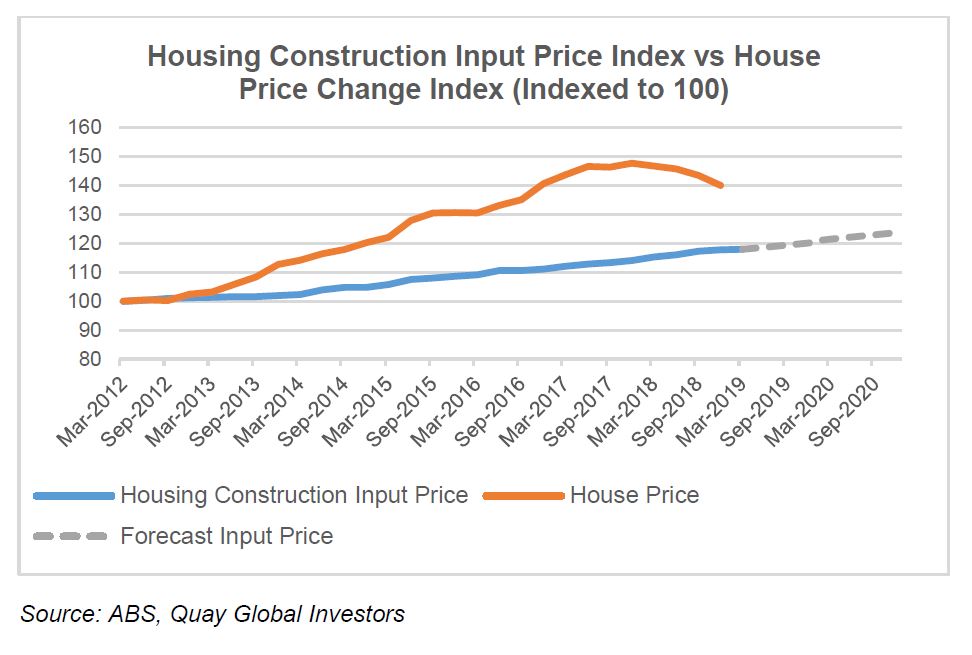

Replacement costs

Overall, housing construction input costs were up ~16% between December 2012 and December 2018. Over the same time period, house prices (based on the ABS house price index) were up ~40% – but more recently, they have been on the decline. Though the gap between house price and replacement cost is large, it is narrowing – particularly as construction input costs continue to increase.

Note this chart assumes that at the starting point (March 2012), prices = cost. However, approvals and completions were near cyclical lows at the time, suggesting prices were less than cost. Land price appreciation since is another factor. If so, then profit motive for developers in the current environment is narrower than the chart below suggests.

Supply response

The above charts show three interesting points about how supply has responded to market prices.

-

Accommodative monetary policy drove housing investment and prices to record levels post 2012. Developers responded by increasing supply, with approvals peaking in 2016/2017.

- This supply response resulted in an oversupply in the market, with completions peaking in 2018 (and expected to remain high in 2019), as prices began to fall.

- Amid declining developer profit margins, poor sentiment, market uncertainty and tighter lending standards, housing approval levels (supply response) have now fallen to a five-year low.

The decline in housing approvals is good news for asset prices (although bad for the economy). Less supply is good for the occupier market, which will stabilise rents and support valuations. But if the decline in approvals (and therefore supply) is sustained, is the market back in balance?

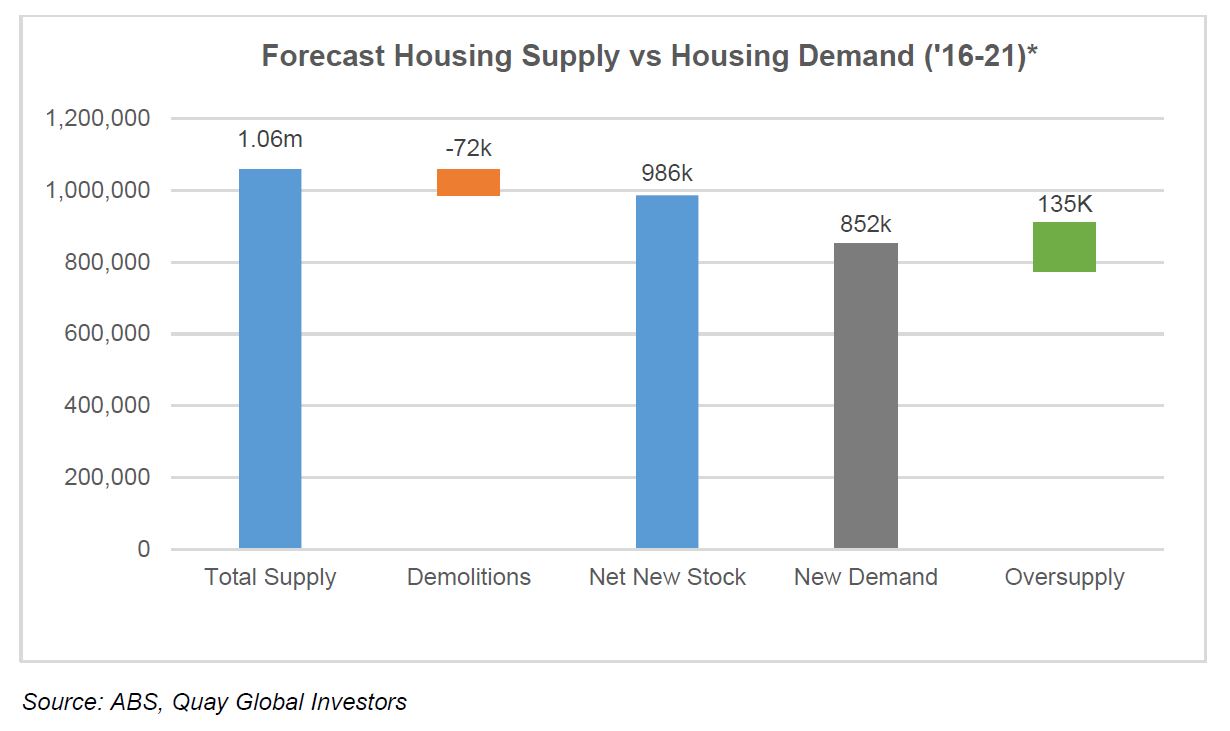

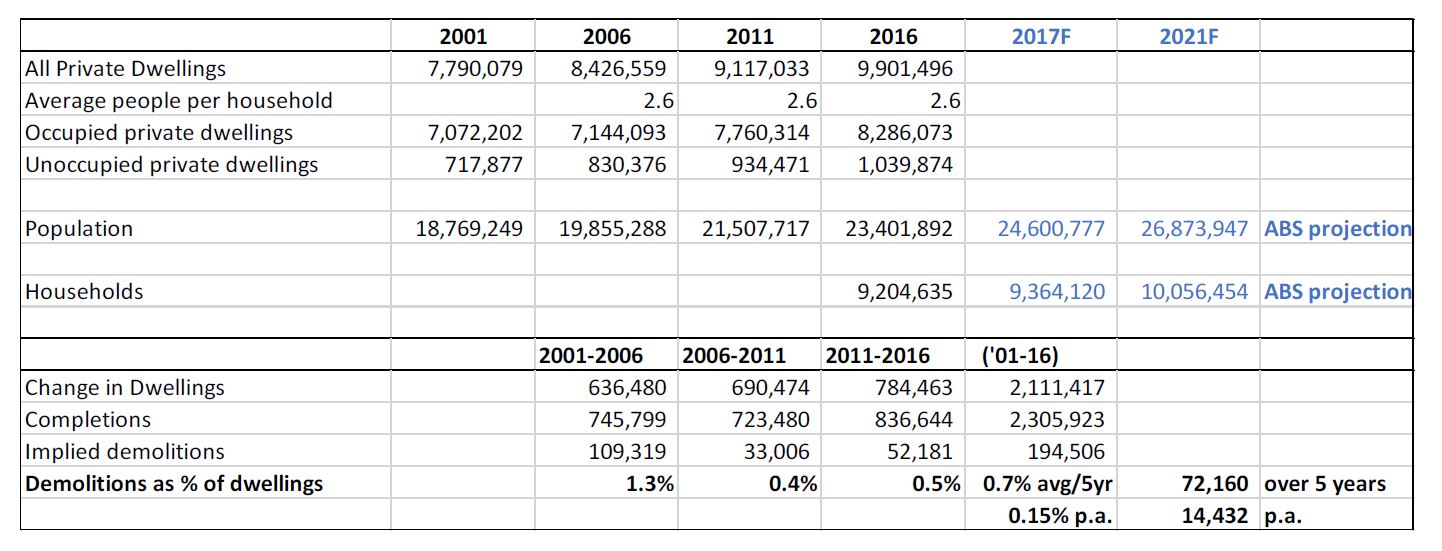

As the following chart shows, even if this bearish sentiment continues to be a headwind for new projects, net new housing supply (derived from ABS housing approvals) will still exceed dwelling demand (ABS projected household growth) in the near term, albeit with the imbalance at a lower level. At the current run rate, we estimate there will be a surplus of ~135,000 dwellings over the five-year period to 2021.

While this may seem bearish, we make two further observations:

- 135k excess dwellings in the context of a 10m housing market is relatively small, and

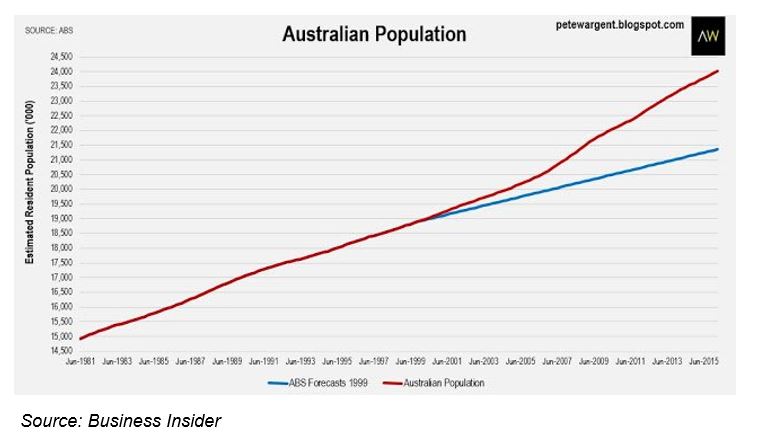

- We note that historically the ABS’s population projections (which are the basis of the household formation forecast) have underestimated the actual growth (see chart). Our calculations estimate a +3% p.a. growth in households (i.e. 1.2% p.a. higher than the ABS’s prediction of +1.8% p.a.) would be enough to absorb the total forecast supply.

Recent history tells us that interest rate cuts have been followed by periods of growth in house prices

While long term pricing for most residential stock is governed by trends in replacement cost, there is no doubt short term stimulus can have a positive impact on near term prices. Now interest rate cuts are firmly on the agenda, the logical question to ask is what impact this will have on near term price.

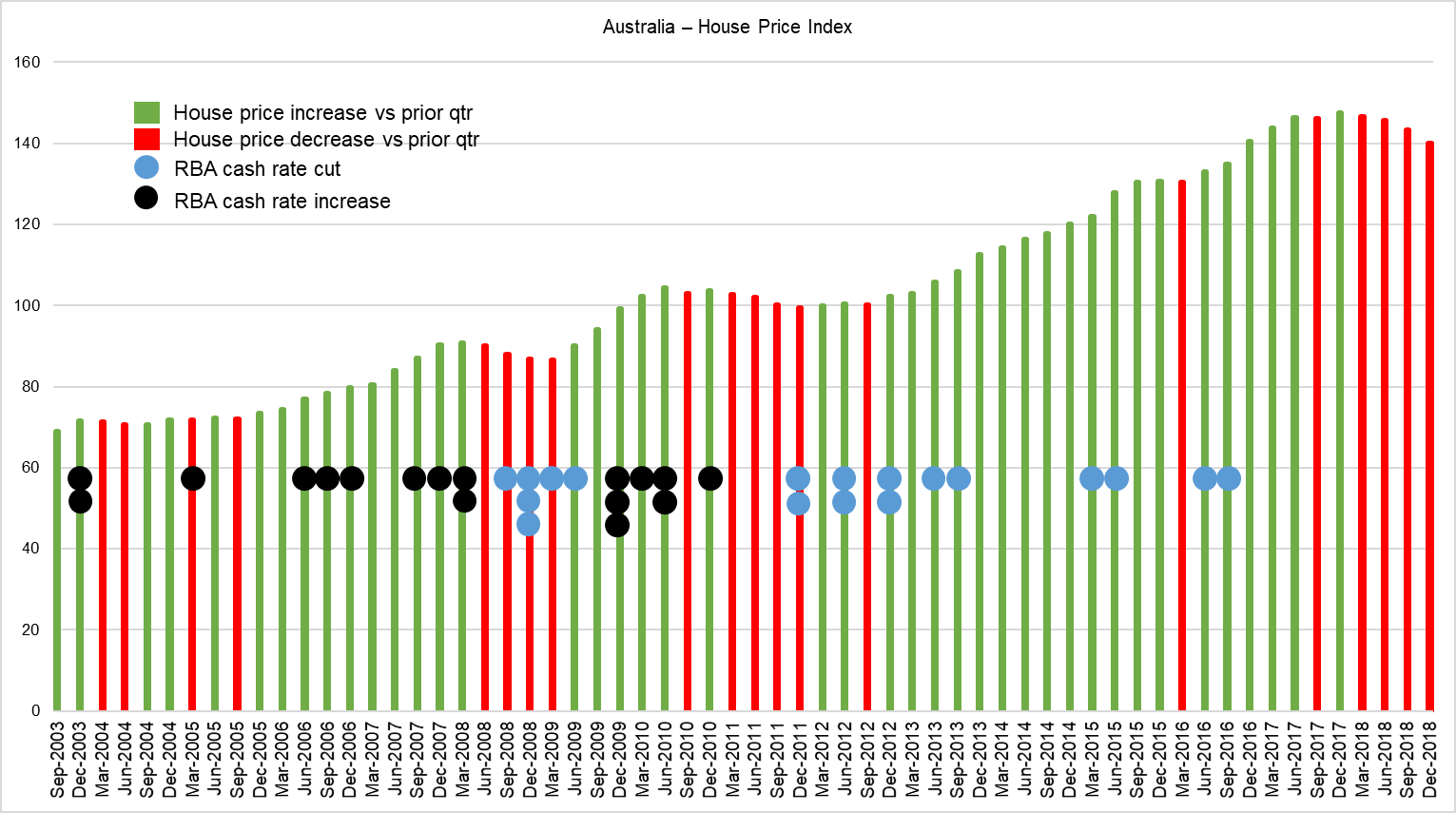

Since 2003, there have been 35 occasions where the RBA has altered monetary policy. On 17 occasions interest rates increased, and 18 times they were cut. The following chart highlights these changes against national house prices.

This chart highlights some interesting historical dynamics between interest rates and house prices in Australia. In particular, following a decision to cut cash rates:

- House prices ended the quarter higher in at least three of the next four quarters. The only exception to this was during the GFC period of late 08 – mid 09.

- House prices were always higher both one and two years on, even during the GFC period.

The chart also shows that between 2012-16, the cash rate was cut 10 times (a total of 2.5%) in periods when house prices continued to trend upwards. This was a policy decision by the RBA to stimulate the economy in response to falling business investment (mainly mining). As a result, residential investment replaced business investment, driving growth in housing with the house price index +47% (2012- 2018). A housing market model published recently by the RBA attributes much of the house price growth in the period since 2012 to these interest rate cuts.

If we were to judge the relationship based solely on these observations, then at least historically there is a clear boost in house prices as result of an interest rate cut.

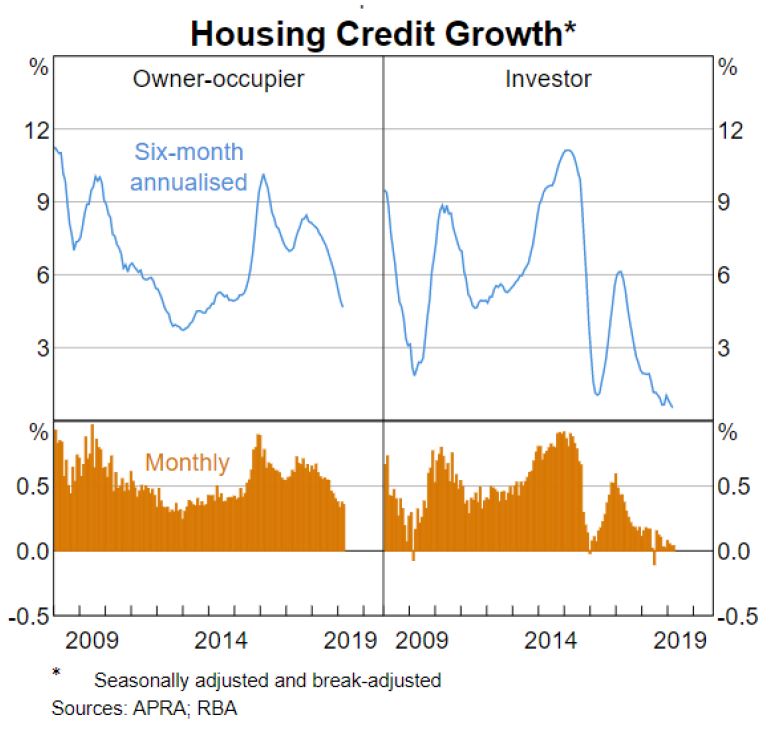

Bank lending: a handbrake on the market?

It has been well publicised that bank mortgage lending has tightened significantly because of the Royal Commission and increased scrutiny on the banking sector. Serviceability requirements, income and expense verification have become more stringent, limiting the pricing and transaction activity of the housing market.

This chart shows the dramatic drop off in credit growth in recent years.

Weak housing credit growth places pressure on bank margins – further, a cut in official interest rates reduces bank returns on cash reserves (another profit headwind). Some may question: how much of future interest rate cuts will be permanently passed onto home owners? While this is a common question, in our opinion, this is not the main issue.

A much bigger restraint on housing is the APRA regulation that requires banks to assess potential borrowers on their ability to manage their loan obligations based on a minimum 7.25% interest rate. This impacts not only the number of people in the market who can obtain loans, but also the size of the loans.

In May 2019, APRA guided that it will review whether to remove this rule and instead let banks assess serviceability based on their own rates (expected to be the mortgage rate plus a 2.5% buffer). Based on a normal discounted mortgage rate of 4.0%, the new buffer will be 6.5%. We believe this change is significant, as house prices are more affected by access to credit than the cost of credit. From a credit availability perspective, such a move is equivalent to three interest rate cuts. This in turn could boost loan growth and housing demand in the near term, particularly as interest rates are lower. We estimate that reducing the stress rate from 7.25% to 6.5% or 6% will increase borrowing capacity by ~11% and ~20% respectively. Most of this capacity could well find its way into house prices in the near term.

Conclusion

Our call for national house price declines in 2017 was well timed. But the market dynamics have changed. The excess price relative to cost has narrowed (reducing developer incentives), recent decline in approvals will move the market towards balance, and the historic relationship between interest rate cuts and prices suggest the market may well stabilise in the near term.

The potential for new APRA guidelines is a big change. House prices rely on credit, and improving credit availability is akin to interest rates cuts (though far more potent). While the housing market may stabilise and recover in the near term, keep an eye on employment, approvals and new housing starts. A return of positive sentiment may encourage developers to oversupply the market once again.

To receive CPD points for reading, view this article on AdviserVoice’s website and complete the questionnaire.

Appendix

Forecast 2016-2021 housing supply vs demand in page 3 was calculated based on the following methodology:

Forecast Housing Supply derived using ABS housing approvals data. Assume all approvals will complete and lagged houses by 9 months (i.e. 9 months between approval and completion) and other dwellings by 15 months. Where necessary, forecasted quarterly future approvals by decreasing actual prior corresponding period approvals by -5%.

Forecast Demolitions: No official figure tracks residential demolitions. However, we can imply the amount of demolitions by comparing total dwellings at previous census dates to completions over the 5 year periods. Refer to table below.

- Total dwellings increased 2.1m over the 15 year period between 2001-2016 (based on census data) compared to completions of 2.3m (ABS). This implies 0.2m in demolitions over the 15 year period, i.e. an average rate of 0.7% of total stock demolished every 5 years, or 0.15% p.a.

- Applying the 0.15% to the 2016 total stock figure of 9.9m, we forecast 72k demolitions (14.4k p.a.) in the next 5 year period ending 2021.

Net New Stock: Forecast Housing Supply – Forecast Demolitions

Forecast Household Demand: Forecast 2021 households (ABS) minus 2016 households (census)

Oversupply: Net New Stock – Forecast Housing Demand