Emerging market (EM) economies are expected to grow rapidly over the next 30 years, attracting huge infrastructure investment.

EMs and infrastructure are natural, complementary investment partners. Rapidly growing EM economies need infrastructure investment to both facilitate and sustain growth. Equally, these assets perform at their best in expanding economies, where robust domestic demand growth drives patronage growth. In addition, infrastructure offers natural protection to some of the key EM risks including the critical one of inflation.

Sarah Shaw, Global Portfolio Manager at 4D Infrastructure, explores the connectivity between EM and infrastructure, addressing why the relationship is so positive. Given this, we believe investors seeking EM equity exposure should consider infrastructure as a portfolio allocation option.

1. EM economic growth: leading to change in the world economic order

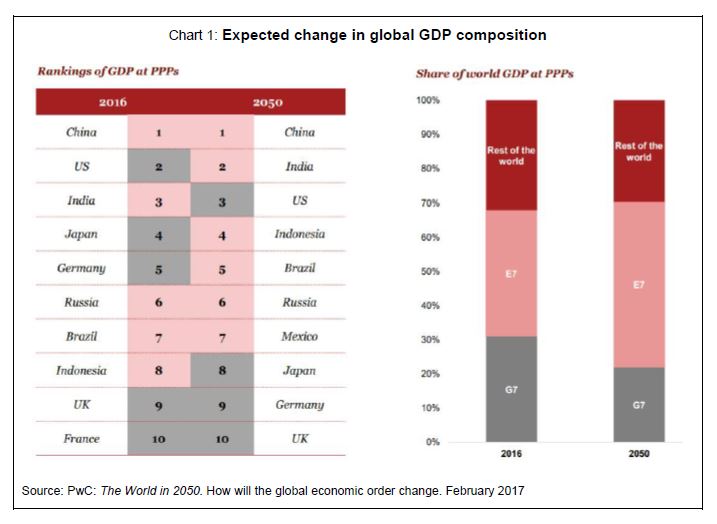

EM economies are expected to grow rapidly over the next 30 years, altering the current world economic order which has been in place for much of the post-World War II period. For example, PwC expects the ‘Emerging 7’ (China, India, Brazil, Mexico, Russia, Indonesia and Turkey) to grow significantly and displace some of the G7’s (Canada, France, Germany, Italy, Japan, UK and US) current share of world GDP (including Germany and Japan).

2. What is driving this change in the world economic order?

As we wrote in Global Matters 17: The insatiable need for infrastructure investment there are several compelling forces driving this change, but here we focus on two critical ones – the emerging middle class; and government policy initiatives such as China’s ‘One Belt One Road’ initiative.

-

The emerging middle class: especially in Asia

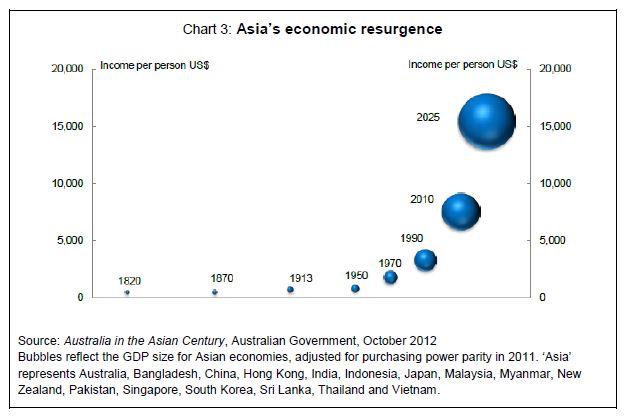

A recurring theme over the past few years has been, and remains, the importance of the emerging middle class. For example, the Brookings Institute believes the global middle class will grow by 160 million people per year for the next five years, with 88% of that growth in Asia. In contrast, the middle class in the US, Eurozone and Japan is only expected to grow at 0.5% p.a.

The consequences of this societal change are significant. This growth in the middle class will help drive the EM economic growth referred to above, as well as the changes in society discussed below. These changes will themselves drive changes in aggregate demand, and the need for new infrastructure investment.

- Middle class and income growth: essential services are indeed essential

China and India have almost tripled their share of the global economy over the past few decades, with growth expected to continue. As personal incomes rise the expected standard of living also rises, triggering a demand for new and improved infrastructure such as the supply of essential utilities – clean drinking water, waste water services and power.

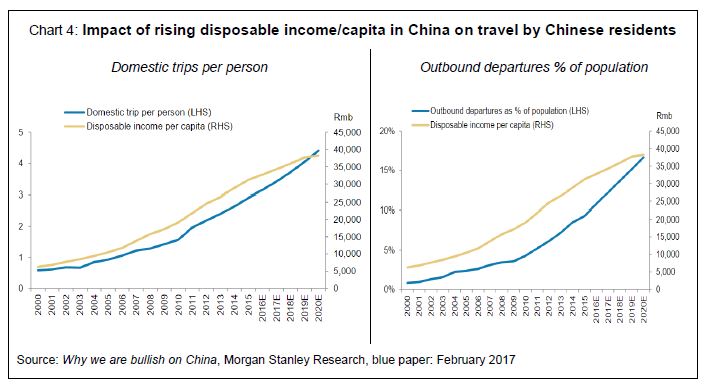

- Middle class and travel growth: airports and ports needed

Studies show that as disposable income grows, so too does the amount of travel undertaken by residents, both domestically and overseas (see Chart 4). China is a perfect example, with less than 10% of Chinese nationals currently holding a passport (compared with approximately 36% of Americans) – yet airports such as Sydney, Auckland and Paris are recording record passenger numbers, driven by Chinese travellers.

This phenomenon is not isolated to China – the trend is expected to continue and be exhibited more broadly across EMs. Mexico is another great example, with domestic air travel growing at double digits. New improved airports/ports/rail will be demanded by these newly affluent travellers.

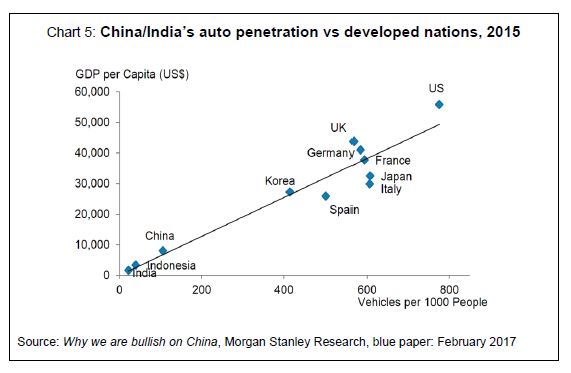

- Middle class and increased motor vehicle penetration: improved road infrastructure demanded

There is a natural correlation between growth in GDP per capita and vehicle ownership. China, India and Indonesia (approximately 40% of the global population) all currently have low levels of vehicle ownership (see Chart 5 below). However, this will grow as each nation’s GDP per capita climbs. As a result, demand for new cars can be expected to be strong, as will demand for new and improved road infrastructure.

To put this in perspective, China’s MV penetration is about 10% – yet annual motor vehicle sales in China have outpaced the US since 2009. An infrastructure investor doesn’t mind what car type someone is driving, as long as they are driving it on their road!

-

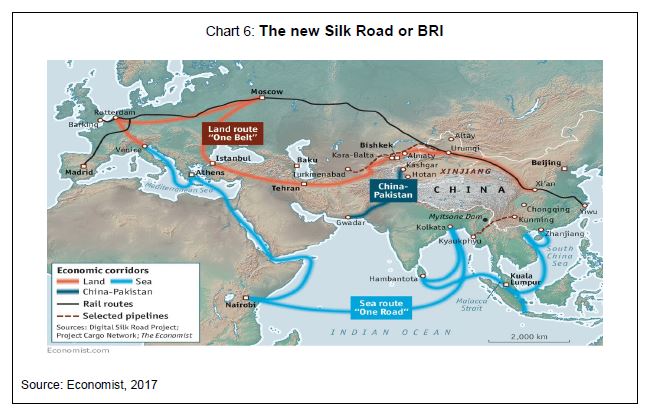

The new ‘Silk Road’: it will transform Asia and propel its growth & infrastructure development

The new Silk Road in Asia, or more formally the Belt and Road Initiative (the ‘BRI’), is a major Chinese foreign and economic policy initiative. Formally, the BRI emphasises five key areas of international co-operation[1]. However, it is the huge investment in infrastructure needed to facilitate the BRI’s trade objectives that has received the most attention. China has signed up approximately 65 countries to the initiative, and is looking to spend around US$600-800 billion over the next five years.

3. EM economies and infrastructure investment: Natural partners

The expected rapid growth in EM economies over the next 30 years will alter consumption patterns in these countries, which will in turn drive new infrastructure investment. This investment then further reinforces that growth and change in consumption.

But the complementary nature of EM economic growth and infrastructure investment goes further. It offers investors access to the domestic demand story while mitigating some key EM risks, thus presenting a very attractive way to gain EM exposure.

Risk is not confined to EMs. However, there are certain key risks in EM that are mitigated by infrastructure investment, namely:

-

Inflation: look for the hedge

A core concern for EMs over the medium term is domestic growth-driven inflationary spikes. The infrastructure asset class provides investors access to the upside of this strong GDP growth while explicitly hedging against inflationary pressure (regulation and contracts provide for an inflation hedge), mitigating one of the key EM investment risks.

-

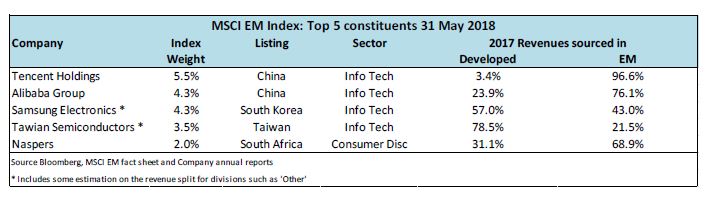

Beware the benchmarks: not all MSCI EM index constituents provide full EM exposure

When looking for EM exposure, an investor needs to make sure they are actually getting EM exposure. Investors seeking access to the EM domestic growth story should be wary of some of the constituents of the MSCI EM index. While some stocks are listed in an EM country, they may have underlying earnings drivers not correlated to EM growth, but rather global demand (for example, Samsung Electronics and Taiwan Semiconductors). Taking Taiwan Semiconductors (see table below) as an example:

- it is listed in Taiwan;

- it made up 3.5% of the MSCI EM index in May 2018 and was the fourth-largest index weight; and

- in 2017, 78% of revenues came from Developed Markets (64% from the USA alone), while only 9% were derived domestically in Taiwan.

So even though it represents a major component of the MSCI EM index, an investment in Taiwan Semiconductors is providing only very modest EM economic exposure. In sharp contrast, EM infrastructure investment provides exposure directly correlated to in-country domestic demand.

Further, as shown in the table below, the MSCI EM offers investors quite high levels of cyclical exposure, with four of the top five stocks being information technology (IT) related. Taking the entire MSCI EM index, more than 80% is in cyclical sectors such as IT (29%), Financials (23%) and Consumer Discretionary (10%), while just 2.4% is in defensive Utilities – suggesting it would be difficult to position for the downside.

-

Local governments: supportive of infrastructure development

EM governments and policy makers recognise the need for improved infrastructure to enable their economies to evolve. As they cannot facilitate all the investment needed, they are supportive of private investment in infrastructure assets to provide the essential services needed to facilitate economic growth, and deliver improved living standards. While EM governments continue to need private sector capital, investors should have confidence that acceptable investment returns will be supported.

-

Distinct infrastructure sub-sectors: Utilities and User pays

Infrastructure offers two macro diverse sub-sectors, which means an infrastructure portfolio can be positioned for all points of a macro cycle. Utilities meet basic needs and are largely immune to macro cycles, making them an attractive defensive, resilient asset class in depressed markets.

By contrast, User Pay assets (toll roads, airports, port and rail) are positively correlatedto macro growth and represent a very attractive investment proposition in buoyant macro environments. Active management of these two infrastructure sub-sectors aims to smooth the volatility of EM investment, again comparing favourably to the MSCI EM which favours the cyclicals.

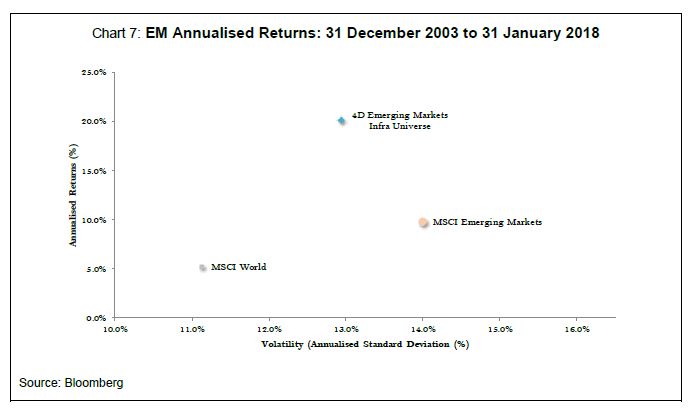

As shown in Chart 7, history supports the view that infrastructure is an attractive way to gain exposure to EMs, offering investors better returns at lower volatility than broader EM equities.

4. Conclusion

EMs are expected to grow rapidly over the next 30 years, attracting a huge infrastructure investment. This is a good thing as EM and infrastructure are natural, complementary investment partners. They reinforce each other in a positive manner, while infrastructure investment can offer natural protection against some of the key EM risks, including the critical one of inflation. Rapidly growing EM economies need infrastructure investment to both facilitate and sustain growth. These assets also perform at their best in expanding economies, where robust domestic demand growth drives patronage growth.

Given these positive characteristics, we believe investors seeking EM equity exposure should consider infrastructure as a portfolio allocation option.