Vancouver Airport. Source: 4D Infrastructure

A cornerstone of our investment process is company management meetings and site visits. These meetings serve several purposes, including providing an insight into management—how they think and run their business—and whether management priorities align with ours as investors. Our Company Quality Grading process involves explicitly ranking company management, so first-hand contact is vital.

The 4D investable stock universe is dispersed broadly around the globe. This necessitates our team travelling widely to call on companies, meet management and conduct site visits. This invariably provides a great insight into not only the specifics of the company being visited, but also a real perspective on what is happening more broadly in the relevant sector, economy and society. We prepare detailed notes after those meetings which capture and relay the key issues and themes of the day.

This is the fourth in our series of Trip Insights, where we share those experiences. It follows a trip in April 2018 when Mark Jones, 4D Senior Investment Analyst, completed an extensive company engagement and calling program in Canada over two weeks, meeting with management teams from Oil & Gas Infrastructure, Regulated Utilities, Renewables, Rail, and Communications Infrastructure across a number of provinces and cities.

Overview

Politics and infrastructure

It is always critical to stay abreast of Canadian politics due to their potential impact on Canadian infrastructure companies. In general, there was cautious optimism in Canada (despite the headlines) that both federal and provincial governments are aware of the benefits to economic activity of enabling increased spend on infrastructure, with most attention (and company visits) focused on oil and gas infrastructure.

Oil and gas infrastructure

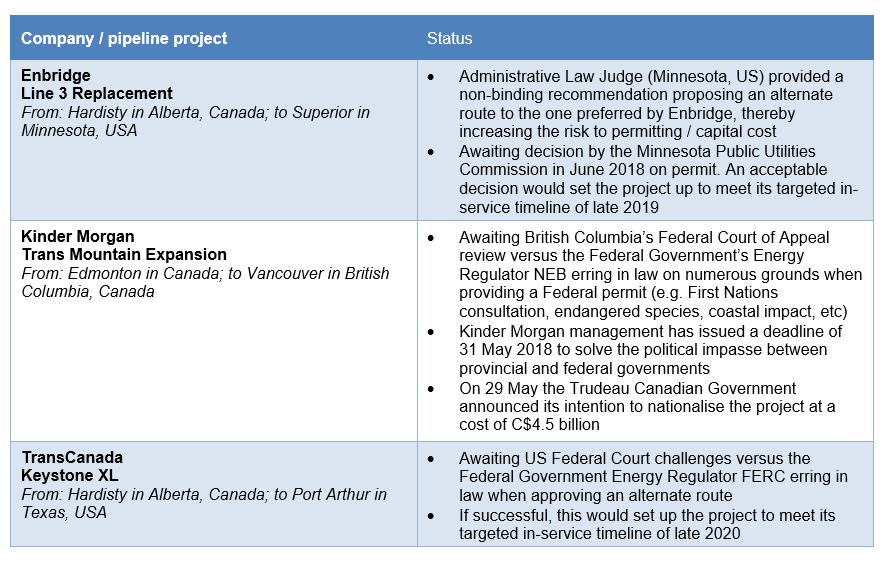

Canadian oil infrastructure companies are facing increased scrutiny and uncertainty in expanding oil pipelines. There are three large oil pipeline expansions being proposed to meet increased supply from oil sands: Kinder Morgan’s Trans Mountain expansion; Enbridge’s Line 3 replacement; and TransCanada’s Keystone XL. All three are delayed due to political and regulatory uncertainty.

Of these, the Trans Mountain expansion project is the most contentious. From an oil and gas infrastructure perspective, this is a gold standard project. It enables diversification away from the US as an end market, and is an essential service for Canadian oil explorers and producers. The political tension comes from British Columbia, where a minority government was elected with a mandate to oppose the project. With the expansion having passed all environment and regulatory hurdles, the only recourse for British Columbia was to challenge the project in the Federal Court of Appeal.

Given the uncertainties, the project’s sponsor, Kinder Morgan, set a 31 May deadline for resolution of the political impasse. Then on 29 May, in a remarkable decision that reflects the importance of the project to Canada, the Trudeau Canadian government resolved the impasse by nationalising the project, agreeing to pay Kinder Morgan C$4.5 billion for the right to do so.

Regarding gas infrastructure, there is an increasing need for more pipeline capacity as evidenced by the weak Canadian natural gas price, presenting an opportunity for Canadian infrastructure companies. In the short term, additional pipeline capacity into the US is being proposed. In the long run, however, this highlights the need for Canada to diversify away from the US as an end market, and the importance of the export of natural gas through liquification (LNG). This is being galvanised through the LNG Canada project – a proposed liquification export terminal in British Columbia.

Unlike the Trans Mountain expansion, the British Columbia government supports LNG Canada – offering tax breaks during construction and granting access to cheaper power. With the final investment decision due before year end, confidence is high that the project will go ahead, providing a market for an incremental two billion cubic feet of natural gas demand and increased need for more gas infrastructure in Canada.

Renewables

Canada’s position as a world leader in renewables has led to the formation of several specialised listed renewable companies, which have observed (and benefited from) the rapidly declining levelised cost of electricity (LEC) for onshore and offshore wind and solar. LEC is the net present value of the unit cost of electricity over the lifetime of a generating asset, and is often taken as a proxy for the average price the generating asset must receive in a market to break even over its lifetime. Reductions in LEC have come from technology gains, most notably increases in capacity.

Rail

Canadian rail companies are experiencing very strong operating conditions, with volume growth above Canada’s GDP growth – Canadian National’s 2017 volumes were up 10% compared to 2016, while Canadian Pacific’s volumes were up 4% compared to 2016. This has led to unintended consequences. Canadian National was negatively impacted on operational indicators such as velocity and terminal dwell, to the point that it curtailed volumes in the first quarter of 2018, ultimately leading to the dismissal of its CEO. Canadian Pacific has faced increased agitation and threat of strikes from the Teamsters union.

Airports

Disappointingly, in April 2018 the Canadian Federal Government decided to shelve its in-depth study of airport privatisation. This goes against a recent global trend whereby airports have been privatised (Japan, Brazil, etc).

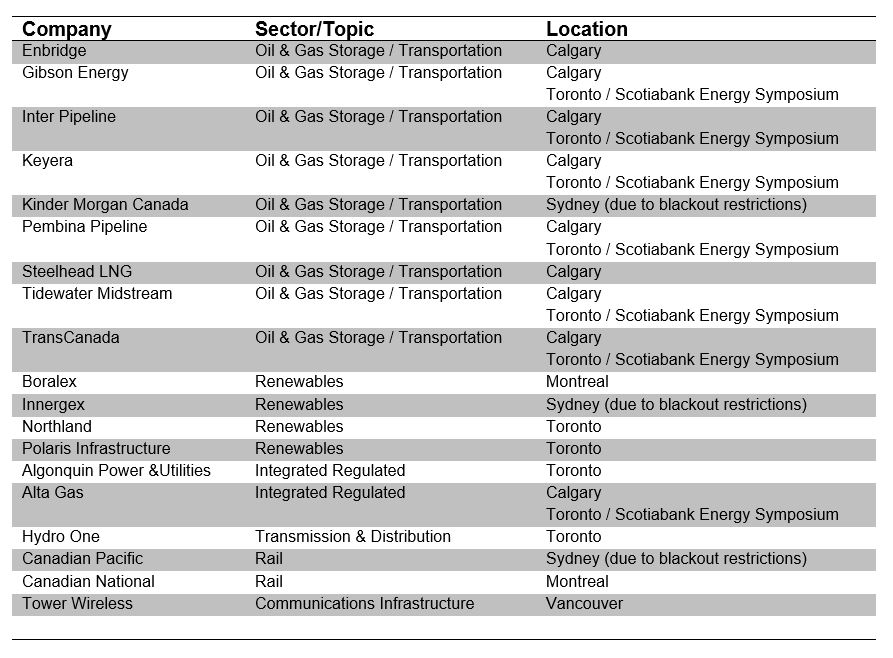

1. Trip Agenda

2. Oil & Gas Transportation / Storage

Meetings were held with the entire Canadian Oil & Gas infrastructure sector through a combination of one-on-one meetings at company headquarters, and attendance at RBC’s Energy Infrastructure Conference in Calgary and Scotiabank’s Energy Symposium in Toronto. The following themes emerged.

Price signals highlight infrastructure constraints and opportunity

In both oil and gas, Canadian explorers and producers receive a discount in price relative to their US peers. While this is influenced by numerous factors, the most pertinent to infrastructure companies is the lack of transport to end markets, highlighting the potential investment opportunity.

Proposed oil pipelines

Alberta’s oil production and supply has been increasing significantly due to oil sands developments. In March 2018, production averaged ~3.5 million barrels per day, representing considerable growth over 2010 when it averaged ~2 million barrels per day. While estimates vary, current oil production is in equilibrium with oil pipeline capacity, with any reduction in capacity causing significant displacement and volatility in Canadian oil ‘netback’ (gross margin to the producer). This has been evident over the past six months, whereby a reduction in oil pipeline capacity (caused by damage to the Keystone pipeline) led to approximately C$20–30 discount in Canadian oil netback.

Canada’s oil infrastructure companies have been proactive in attempting to progress three large oil pipeline expansions, which would collectively add more than 1.7 million barrels per day in capacity. The status of these projects and possible risks to their timing and execution are detailed below.

Of these projects, the Trans Mountain expansion is the most contentious. It is a proposed oil pipeline twinning an existing 1,150-kilometre pipeline between Alberta and British Columbia, aiming to increase capacity of the system from 300,000 to 890,000 barrels per day.

From an oil & gas infrastructure perspective, this is a gold standard project. The existing and proposed expansion of the Trans Mountain pipeline enable diversification away from the US as an end market. It is an essential service for Canadian oil explorers and producers who have collectively signed on for 15-20 year take-or-pay contracts, escalating at inflation, to underpin the significant capital (approximately C$7.4 billion last estimate) being deployed.

The political tension comes from the Canadian province of British Columbia, where a new minority government – a coalition between the New Democratic Party and the Greens – was elected with a mandate to vehemently oppose the Trans Mountain expansion. With the project having passed all environment and regulatory hurdles, the only recourse for British Columbia was to challenge the project in the Federal Court of Appeal, launching 19 separate legal challenges to the issuing of the federal permit. With Federal Government support for the project unwavering, yet somewhat ineffectual, this has led to perverse outcomes such as the Alberta government proposing to selectively exclude imports from, and exports to, British Columbia – thereby eroding the benefits of federalism.

Given the uncertainties, the project’s sponsor – US-based oil & gas infrastructure player Kinder Morgan – declared it was facing an ‘unquantifiable risk’ in continuing to develop the project, and set a 31 May deadline for resolution of the political impasse.

In general, there was cautious optimism that all three oil projects will go ahead because:

- they are essential services required by the Canadian oil sands industry to remain competitive;

- the Federal Governments in both Canada and the US have reiterated their support for all projects; and

- the companies involved have credible environmental, social and corporate governance track records and reputations.

Then on 29 May, in a truly remarkable decision that reflects the importance of the Trans Mountain expansion project to Canada, the Trudeau Canadian government decided to resolve the impasse by nationalising the project, paying Kinder Morgan C$4.5 billion for the right to do so.

Proposed gas pipelines

In the gas market, similar themes were evident, with Canadian natural gas trading at a steep discount relative to Chicago natural gas prices over the border because the Canadian gas producers are unable to get their product to market due to the lack of gas pipeline infrastructure.

Much like oil, gas production / supply from Alberta and British Columbia has been increasing significantly due to shale gas plays such as Montney and, more recently, Duvernay. Gas production in Alberta / British Columbia in March 2018 averaged approximately 16 billion cubic feet/day compared to 14 billion cubic feet/day in 2010. Canadian gas infrastructure companies have been on the front foot in increasing gas processing and pipeline capacity, with many companies in the sector increasing capital expenditure budgets relative to the levels spent over the past few years. Open seasons from TransCanada with its Nova Gas Transmission pipeline system, and Pembina Pipeline / Enbridge’s with its Alliance pipeline system, will be beneficiaries with increased capital expenditure aligning to stronger growth in future earnings. In the short term this increases the capacity of natural gas export to US by approximately two million cubic feet per day.

In the long run, this increase in gas supply also predicates the need for Canada to diversify and export its natural gas to global markets, rather than being captive to the US market alone. Highlighting both the opportunity and the lack of execution to date, Canada’s National Energy Board has approved 35 export licenses for liquefaction of natural gas (LNG) through the LNG Canada project – a proposed liquification export terminal in Kitimat, British Columbia sponsored by Shell, PetroChina, Kogas, and Mitsubishi. Meeting with one of the proposed licensees, Steelhead LNG, the comparative advantage of natural gas being exported from Canada was highlighted, namely:

- as extracted from the Montney / Duvernay shale gas basins have large reserves, and are in the lowest quartile of the cost curve;

- gas transport from the West Coast of Canada has much shorter shipping distance to Asian markets (approximately 10 days) relative to the US Gulf Coast (approximately 22 days), with no reliance on the Panama Canal; and

- strong government support at both provincial and federal level, providing tax incentives and concessions.

Highlighting the vagaries of politics, unlike the Trans Mountain expansion the British Columbia government supports LNG Canada – offering tax breaks during construction and granting access to cheaper power. LNG Canada involves capex of ~C$40 billion associated with both the liquefaction facility and the pipeline required to transport natural gas from Alberta. With the final investment decision due before year end, confidence is high that this project will go ahead, providing a market for an incremental two billion cubic feet of natural gas demand.

Given the above, and increasing consensus over the need for ~100 billion cubic feet/day of incremental gas supply to Asia, all Canadian gas infrastructure companies were very supportive and confident there would be one to many Canadian LNG facilities, highlighting this would in turn lead to increased demand for infrastructure such as gas processing, pipeline and storage.

Balance sheet and capital structure matters

Despite capital expenditure increasing, listed Canadian oil and gas infrastructure companies have broadly underperformed over the past 12 months. One of the reasons is concern over balance sheet and capital structure – a recurring theme in meeting with companies. While difficult to perfectly isolate, companies with higher levels of leverage and more complex capital structures have underperformed more than their peers.

Enbridge and TransCanada management teams were keen to emphasise initiatives to de-lever balance sheets through capital recycling. This should be broadly supportive, or indeed accretive, to earnings if there is an improvement in the quality of assets being divested and re-invested. In both Enbridge and TransCanada’s cases, infrastructure assets such as field, gas gathering and processing, and contracted generation are being divested with the capital generated recycled into higher quality pipelines and laterals. Combined with the fold-in of sponsored vehicles, this will improve transparency of earnings.

3. Renewables

Meetings were held with the entire Canadian Renewable sector through one-on-one meetings at company headquarters, or conference calls from Sydney if the company was in a reporting blackout.

Canada’s position as a world leader in renewables (in 2016, 66% of electricity generation in Canada was renewable) has led to the formation of several specialised listed renewable companies including Boralex, Innergex, Northland Power and Polaris Infrastructure. Collectively the renewable companies have observed (and benefited from) the rapidly declining levelised cost of electricity (LEC) for onshore and offshore wind and solar. LEC is the net present value of the unit cost of electricity over the lifetime of a generating asset, and is often taken as a proxy for the average price that the generating asset must receive in a market to break even over its lifetime.

Reductions in LEC have come from technology gains, most notably an increase in capacity. As evidence of this, in offshore wind, the largest wind turbine manufactured by General Electric can now generate 12 MWh (the equivalent of enough electricity for approximately 4,000 homes). The ability of renewables to compete with other forms of electricity generation has led to Canadian renewable companies entering into new markets beyond Canada – most notably France (due to a common language), the UK, Germany, Netherlands, and even emerging markets such as Chile and Nicaragua. Markets such as France have particular appeal due to the structure and level of competition underpinning earnings growth over the short and long term.

4. Rail

Meetings were also held with the entire Canadian Rail sector through one-on-one meetings at company headquarters, or conference calls from Sydney if the company was in a reporting blackout.

Canadian rail companies are experiencing very strong operating conditions, with volume growth above Canada’s GDP growth – Canadian National’s 2017 volumes were up 10% compared to 2016, while Canadian Pacific’s volumes were up 4% compared to 2016. This has led to unintended consequences. Canadian National was negatively impacted on operational indicators such as velocity and terminal dwell, to the point where it curtailed volumes in the first quarter of 2018, ultimately leading to the dismissal of its CEO. Canadian Pacific has faced increased agitation and threat of strikes from the Teamsters union (more than 75% of Canadian Pacific’s workforce is unionised).

While curtailment of volumes transported has led to the risk of customer churn and substitution from rail to truck, more broadly it has also re-raised the spectre of government intervention. The influential Grain Growers of Canada industry body is very disappointed with the first quarter 2018 performance of the rail companies, and the resultant growing backlog of wheat, barley and other products. In 2014, the Canadian Government legislated the Fair Rail for Grain Farmers Act which prioritised grain above competing volumes. This Act had a sunset clause, and while repeat legislation is not currently being proposed, it does attract unwelcome attention to rail performance when the current Canadian government is legislating bill ‘C-49’ with the aim of modernising Canada’s transport – including introducing additional competition to its rail sector and potential financial penalties for curtailment.

Notwithstanding this, there are many reasons to remain positive on Canadian rail stocks. The outlook for volume growth remains robust across many segments, including:

- intermodal from Canadian seaports capturing market share from US seaports (mainly due to efficiencies provided by rail access);

- metals and minerals from fracking sand for shale gas; and

- hydraulic fracturing and crude by rail from pipeline constraints.

Some of these tailwinds are short-run, with vigilance required as the acting CEO of Canadian Rail so aptly surmised: ‘Oil companies would get married to pipelines, but they only date the railroad.’

5. Airports

Disappointingly, in April 2018 the Canadian Federal Government decided to shelve its in-depth study of airport privatisation. This goes against a recent global trend whereby airports have been privatised (Japan, Brazil, etc). Canada’s largest airports are currently managed by not-for-profit, non-share capital corporations called ‘airport authorities’ that pay rent to the Federal Government, which maintains ownership of the land and assets. Prior to this policy change, it was thought the privatisation of airports could have been used by the Federal Government to generate and recycle capital on a needs basis. The independent Canada Infrastructure Bank, which manages C$35 billion but is yet to invest in any infrastructure projects, was hoping for a recycling strategy to be adopted to allow it to deploy some of its capital.

Download a copy of the article here.