Key points were:

- general sentiment from many investors was “we are long in the cycle”, as many questions focused on signposts which indicated any type of downturn:

- this concern related more to Storage and Apartments given both sectors have performed strongly in recent years;

- Manufactured Housing occupancies have yet to reach prior cycle peaks – suggesting more outsized growth in the short term;

- industrial landlords continue to push the e-commerce theme enthusiastically. Supply is emerging, but not keeping up with demand;

- the Mall landlords defended the industry, believing the e-commerce threat has been overplayed;

- in Health, the main concerns are the same – supply in assisted living, and risks due to the changes in Medicare payments and the impact on nursing facilities. Nursing aside, the long-term thematic is compelling; and

- Data Centres – Demand is very buoyant as is sentiment towards the sector. Many of the operators remarked that they believe the industry is at the start of an outsourcing trend.

Below we discuss key themes in more detail.

Manufactured Housing

Manufactured Housing (MH) is attractive because it exhibits an incredibly resilient earnings stream through cycle owing to wide appeal and affordability. Additionally, it is a beneficiary of the ageing baby boomers seeking lifestyle or downsizing their housing needs.

Of the 50,000 MH communities that exist in the United States, it is estimated that only 3,000 are investment grade. The two major listed REITs (ELS and SUI) own approximately 10% of this investment grade stock, implying a long runway for acquisitions and development growth.

It’s a similar story with Recreational Vehicle (RV) parks, with only 1,200 of 8,000 private campgrounds in the United States being regarded as investment grade.

Investment grade properties are regarded as having sufficient scale with regard to size and with superior locations.

For development, it is really only land adjacent to existing communities that offer viable opportunity due to the long lead time to reach stabilisation and the ‘not in my backyard’ attitude towards new affordable housing communities. ELS own 6,000 acres adjacent to their properties, which could add between 60,000-70,000 sites, representing almost a 50% increase in existing assets over 10+ years.

90% of tenants who locate an MH in ELS’s communities are cash buyers, generally using the sale of the current home as the equity for purchase. The high proportion of cash buyers, combined with the low cost of manufactured housing, lends to ELS’ and SUI’s ability to continue to increase land rents.

The Fund is invested in both ELS and SUI and we came away from our meetings very comfortable with our exposure to this sector of the real estate market.

Multifamily

The messaging from all multifamily REITs has been consistent – the lower quality ‘B’ type properties have been outperforming A-quality apartment buildings, as the increased supply in marquee markets like San Francisco and New York are really impacting the upper end of the apartment market. Houston, which is suffering from a weak economy following the decline in oil prices, also faces the prospect of increasing supply. While it wasn’t discussed widely, we were very interested in the sustainability of rent growth into the future, and left feeling quite comfortable with Multifamily REIT’s ability to drive increased rents over time.

San Francisco supply coming – but next year looks better

Essex, which has the highest proportional exposure to San Francisco of all the listed REITs, suggested supply delivery in Northern California was focussed in in the second and third quarter this year. These new developments offer 6-8 week incentives, bringing down new lease rates from +4% in April to +3% in May.

Essex also said the supply coming in the northern summer is limited, with management expecting 2017 supply 30% lower than 2016. In talking about how resilient their Seattle market has been in 2016, they noted that apartment rents are quite simply determined by unit demand and supply. Better than expected job growth in Seattle allowed good absorption of supply, which led to better than expected rent growth. Construction labour in Northern California is lacking, as is mobility. This has been increasing construction costs, and therefore reducing development yields. This supports our investment thesis of rising construction (replacement) cost for well-located apartments.

Houston – short-term headwinds

Initial expectations of 50,000-60,000 new jobs in Houston will prove to be overly optimistic, with forecasts reduced to 10,000 new jobs. With 20,000 new apartments emerging in Houston, there is near-term pressure. Market leader Camden Property has one project that will undergo lease-up in 2017. They still believe Houston will have flat revenues in 2016, and management expect a slight negative in the second quarter results. On the plus side, market weakness has meant that new multifamily development starts have ceased in Houston. The existing new supply attracts 3-month free rent concessions to lure tenants.

Will affordability limit further rent growth?

One of the major concerns has been deterioration in ‘affordability’ after years of strong rental growth. Most apartment managers did not see affordability as a headwind.

- Aimco management argues this apartment cycle will be longer than normal, reminding investors the market caters for more than just millennials. Cashed-up baby boomers are also returning to apartments as they downsize and seek cosmopolitan lifestyle benefits and a ‘pied-à-terre’ away from the suburbs.

- Mid America Apartments believe their rent-to-income ratio across the portfolio is between 18-19% (which is pretty low by global standards), so while they have room to expand these ratios, they’re also seeing income growth among their tenants which they believe will keep their rental increases sustainable.

- In Northern California, rent-to-income ratios normally sit between 25%-26%, with the highest being 33% in the early 2000’s. They’re currently 28%. In Southern California and Seattle, they’re usually in the low 20’s with minimal variability. They haven’t seen rent-to-income ratios stray from these levels.

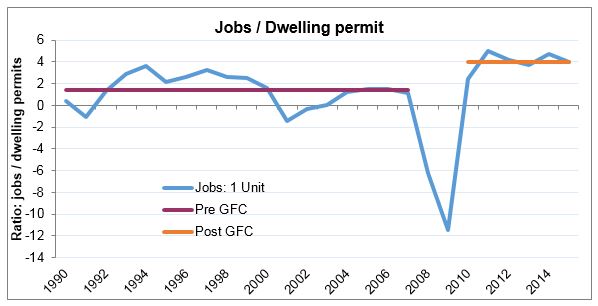

- Some of these comments are at odds with the macroeconomic environment as wage growth since the financial crisis has been near zero in real terms while rental growth has been strong. However, the structure of the housing market has changed. Indeed, the statistics still show that the ratio of jobs to dwelling permits still at elevated levels (4 jobs per dwelling approval, versus just under 2 jobs pre-GFC). This either indicates undersupply, or more wage earners per household. Either way, it paints a positive picture for ongoing rental growth.

Healthcare

REITs with meaningful Medical Office Buildings (MOB’s) exposure tended to be mostly positive, while those with greater Skilled Nursing (SNF) exposures were mixed. Senior housing supply and NOI growth outlooks were also prominent, with managers trying to put their specific portfolios into context as it related to supply impact. We came away from our MOB-focused meetings feeling good about the companies’ ability to generate 2.5%-3% SS NOI growth.

Care Capital (CCP) is at the centre of the shift from fee-for-service to episodic payments (bundled model). Key to their success is backing the right operators to minimise the readmission rate – and hence attract the support of wider health care systems (Hospitals). Indeed, the CMS has a target of 50% of reimbursements into a bundled model by 2018. This makes integrated care important, controlling the post-acute process to control the data. This allows operators to monitor rehospitalisation rates. Does this mean that more or less people will skip the SNF and move into home health? As a ratio, probably yes, but the absolute numbers are growing which is supportive of the entire industry.

The demographics are still compelling – and will be more so post 2018, as the baby bust gives way to a baby boom. At the same time, there has been a decrease in skilled nursing beds! This sector will present some excellent opportunities in the years ahead.

In Canada, supply of retirement residences has been slow for the last 2 years, which is the opposite of 4-5 years ago. Alberta is undersupplied at the present time, but development is occurring in Calgary. Undersupply was caused by elevated construction costs whereas the resources boom priced-out a lot of labour. This trend will reverse as there are discussions of larger developments in Ontario and Quebec. One private operator announced a $1bn development pipeline. Quebec is cheaper than Ontario, and has 18% penetration versus 5% in Ontario – lending to the fact that seniors’ apartments operates under a simple rent model in Quebec.

Industrial

We met with three Industrial operators at NAREIT – US-based STAG and DCT, as well as Canadian REIT Pure Industrial. All companies were quite upbeat on prospects, with DCT telling us that despite elevated construction levels as speculative developers are in the market, there is still ‘years’ worth of demand for industrial space.

In Canada, Edmonton has stabilised from a leasing perspective according to Pure Industrial. Vancouver remains expensive – management quoted $150psf land and build. Toronto is also tight – with cap rates in the ‘low to mid 6's’ and 2% vacancy. Banks in Canada are lending 75-85% of cost for construction loans, with no prelease required. This has us a little concerned.

Many US landlords believe that industrial is a different asset class today, as the rise of e-commerce has created a large amount of demand. In the past, most tenants focused on cost per foot and were therefore price sensitive. Now they’re looking at in-fill locations, and believe there are good prospects for experienced industrial operators. But this view was not unanimous for all landlords – some suggesting the e-commerce story is being overplayed.

We see the enthusiasm for the Industrial/e-commerce story in stock prices. We like the space, but remain disciplined on pricing – acquiring our effective exposure below replacement cost (ex-land). To be honest, there are not many to choose from based on this metric.

Storage

Public Storage (PSA) set the scene early by commenting supply is accelerating across all markets. They continue to observe that with prices well above replacement cost, why wouldn’t you build? For Quay, these types of comments set off alarm bells.

Storage has had a terrific run over the past three years – and the Fund has benefited. For most of our meetings, the theme of supply was ever present.

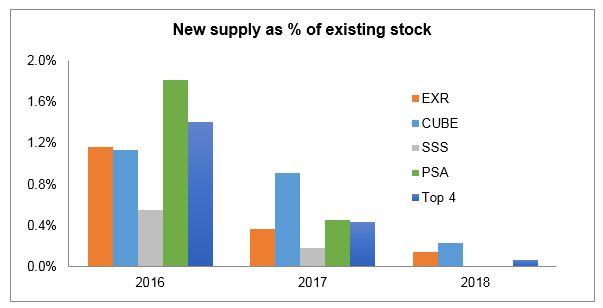

The problem for the industry is there is no one reliable measure on storage supply. Information is almost always anecdotal, but this too poses some problems since storage is really a ‘3-5 mile business’, and the public operators only account for 14% of the whole market.

Sovran Self Storage (SSS) and Extra Space (EXR) believe there are around 600-800 facilities of new supply a year (1.7% of total stock). Sovran has a unique approach to estimating supply. First, management look through notices and local government on any permits for storage within a 5-mile radius of Sovran’s properties. Secondly, self storage locks and doors are somewhat unique – so Sovran often survey the manufacturers of these items to estimate the rate of change (growth) in these items – which are necessary to deliver new supply.

Most operators argue the zoning entitlement process remains very difficult. Storage is hard to approve because it doesn’t employ many people and it doesn’t generate local sales tax. As can be seen from the chart below, data from public listed storage REITs highlights development as a percentage of existing stock is in line with national estimates c1.7% of stock. To put that into context, UK storage supply increased +5% in 2015.

Student Accommodation

We had a meeting with EDR and were quite impressed. Around 30% of NOI is from on-campus accommodation. This is important since on-campus accommodation doesn’t get a lot of competition. The remaining NOI is from properties within a half-mile of campus.

We also asked about EDR’s One Plan development solution for university accommodation. Normally, there are 2-4 bidders for on-campus projects. Terms of agreement are reached with the universities, with 60-75 year ground leases tied to revenue. Management said they like small base rents and the rest of the payments tied to revenue. The university has the option to buy EDR out on the project.

The big theme was the runway for student accommodation upgrade across the US is enormous. There are only two credible operators with the track record and financial capacity to deliver – and a vast majority of US university campuses fast becoming obsolete. Universities compete for students – and offering ‘best in class’ accommodation is becoming a strategic priority.

In the short term, both listed operators (EDR and ACC) are probably over-bought. But the long-term story remains compelling.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.