These issues are exacerbated by comments from foreign credit rating agencies that “rate” Australian creditworthiness. Moody’s recently raised concerns, stating that:

“Although Australia had a favourable budget position relative to other countries with AAA credit ratings, Moody’s noted Australia’s Government debt had risen to 35.1% of GDP in 2015 from 11.6% of GDP 10 years earlier.

“We expect Government debt to increase further to around 38% of GDP in 2018,” it said. Climbing Government debt is “a credit negative for Australia”, raising the prospect of a credit downgrade in future.[1]”

Across the political and media spectrum, the consensus states Australia needs to “repair the budget” to maintain its current credit rating or bad things will happen. But does a credit rating for a sovereign currency issuer like Australia even matter?

Since the Australian Government pays its bills in Australian dollars, what do the ratings actually mean?

Australia is a sovereign currency issuer. Moreover, the local currency is non-convertible. That is, there is no price guarantee the currency can be converted into gold or any other currency.

In this respect, Australia is no different to the USA, Japan, UK, Canada, New Zealand, Switzerland and Norway. But we are different to the European currency union (France, Germany, Greece, Italy etc.) who are effectively tied to a currency peg.

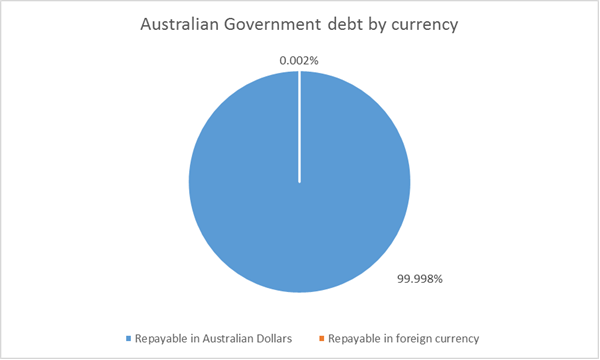

The Reserve Bank of Australia (RBA) issues Australian dollars. The Australian dollar is not issued or supplied by any other nation or bureaucracy.[2] This makes the idea that a credit rating agency determines whether we can “pay our bills” denominated in our own currency – hard to reconcile. Especially considering that 99.998% of Government debt (deliberately not rounded) is denominated in Australian dollars (see following chart).

Source: AOFM[3], Quay Global Investors

Foreigners own a large percentage of government bonds – if they sell, will it raise interest rates and crash the bond market?

Despite the fact that nearly all of the Government’s debt is denominated in Australian Dollars, non-residents own approximately 63.5% of outstanding Australian Government Securities (AGS)[4]. Prior to acquiring a bond, buyers must first have Australian dollars to settle the purchase. Foreign governments and institutions end up with Australian dollars because they run trade surpluses against Australia.

What they do with those dollars is completely up to them – subject to rulings by the Foreign Investment Review Board (FIRB). They can sit with the cash, buy shares or property, or they can choose to own a riskless government bond.

If they own government bonds and then decide to sell their bond holdings and forgo that interest premium, then that’s their loss. But as long as foreign entities incur a trade surplus with Australia, they will keep accumulating Australian dollars – they want those dollars as a function of their trade position.

Furthermore, if bond yields begin to increase from any near-term selling pressure, a significant trading profit emerges for those who bought at the resultant higher yields. All bonds eventually mature. In Australia, this means that bonds qualify as ‘Approved Securities’ by the RBA for liquidity. That is, the RBA is a willing buyer of government bonds as part of its repurchase (repo) facility with the banking system. In short, bonds turn to cash – and owners of the bonds end up receiving that cash rate. For a detailed discussion on this point, please see Appendix A.

When bond yields move significantly higher than the cash rate, it is a very profitable trade for investors to sell cash and buy bonds (spread) – since the credit risk of the bond is the same as the RBA – the entity that issues the currency!

Even the European Central Bank, in a discussion paper, now admit that central banks can’t go broke.[5]

It is interesting to note that during 2015, Chinese ownership of US government bonds declined[6] – and despite all the hand-wringing that such a move would prove to be disastrous for the US bond market, long-dated yields are lower today than at the beginning of the year. Australia should take note.

But if the Government doesn’t “fix the budget” and continue to borrow, won’t it crowd out the bond market and increase interest rates?

This type of argument gets causality in reverse. The government deficit actually equates to a non-government surplus. Dollar for dollar. This is an accounting reality.

When the Government runs a deficit, it adds to the net financial assets of the non-Government sector. Government spending provides the funds for the non-Government sector to buy the bonds! For more on this please see Appendix A of this paper.

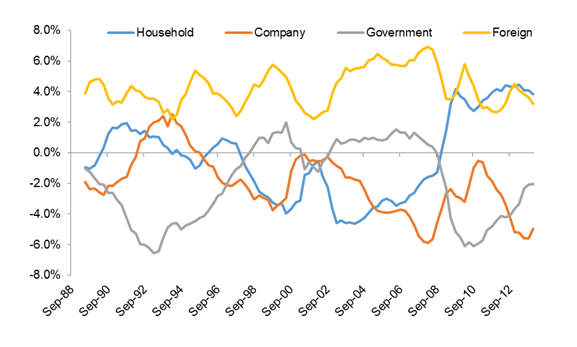

This can be observed by charting Australia’s sectoral balances, sourced from the Australian Bureau of Statistics (ABS). The chart below breaks down the financial surplus/deficit for each sector as an annual average percentage of GDP: Government, Business, Households, and Foreigners. Since one sector’s spending is another’s income, these four sectors add to zero – always.

Source: ABS National Accounts, Flow of Funds Matrix (cat 5232.0), Quay Global Investors

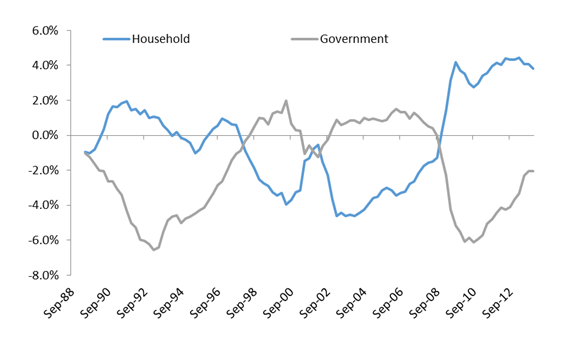

Over time, business investment generally offsets foreign savings. If we exclude these two components from the chart, we find a very interesting inverse relationship.

Source: ABS National Accounts, Flow of Funds Matrix (cat 5232.0), Quay Global Investors

The evidence is clear. The budget position is a big driver of household savings patterns. Since the financial crisis, the Government has returned to deficit, adding to household savings. These savings accumulate in bank accounts and superannuation funds, which are used to buy government bonds, among other assets. Of course, not everyone uses savings to buy a bond. They may buy shares, or property, or just leave it in the bank. But the sellers of shares or property, or indeed the bank, will have the new liquidity to buy bonds.

This means there is always enough “money” to buy the bonds, regardless of the size of the deficit. The yield of the bonds simply reflects an indifference point between owning duration (bonds) and cash.

When the Government promise fiscal surpluses, what they are really promising is to reduce private sector savings.

The policy of “budget repair” is highly problematic given wage earners are required to add to savings by contributing to superannuation funds. In short, it is unlikely the Government will return to any meaningful surplus for a very long time. This is because the national superannuation policy is working against it[7]. But does that matter? Do ratings agencies determine Australia’s credit worthiness?

Rating agencies track record for sovereign credit is patchy

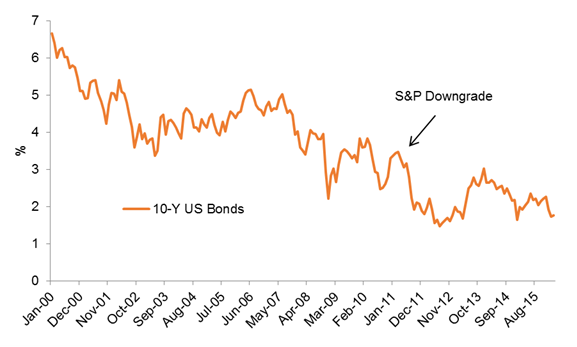

On 5 August 2011, Standard & Poor’s (S&P) downgraded US debt by one notch to AA+ from AAA. At the time, US 10-year bond yields were 3.1%. Today they are approximately 1.8%. Clearly, the effect of the downgrade was very different to what we would expect to a corporate bond. The question needs to be asked, is something else going on here?

Source: Bloomberg, S&P Ratings, Quay Global Investors

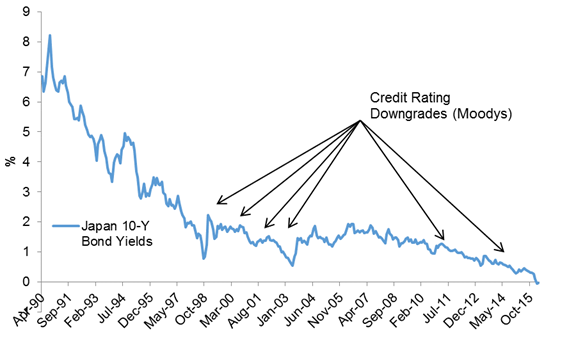

For a while, Japan has been the country widely seen due for the next “debt crisis”. Ratings agencies have been vigilant in downgrading Japanese sovereign debt over the past 20 years. Despite this, bond yields have fallen. Today, investors are prepared to pay for the Japanese Government to take their money!

Source: Bloomberg, Quay Global Investors, Moody’s Ratings

But Australia is different, right? Aren’t we a small nation reliant on foreign funding? We can’t compare ourselves to the US dollar – the world’s reserve currency? Or Japan, which has a huge savings rate?

As far as the structure of the monetary system is concerned, Australia is not so different. Australia’s financial system is very similar to the US. The currency is issued by electronic keystrokes by the central bank. In that respect, the AUD is no different to the “reserve currency”. A spreadsheet in Australia works just as well as a spreadsheet in the United States.

And as for Japan’s savings rate – as discussed above, that is simply a function of the deficit. Ongoing Japanese deficits have resulted in large household savings. The laws of accounting apply equally in Australia.

So deficits don’t matter? Does “printing money” mean we will become the next Zimbabwe?

Deficits do matter, but not in the context in which they are often portrayed.

The Government can issue currency to acquire the resources it needs to meet its economic and social goals. However, if those resources are already fully utilised by the non-Government sector, consumer and labour prices rise, causing inflation. Rising inflation and low unemployment is a sign the deficit is too large (or surplus is too small). Conversely, rising unemployment and persistent low inflation is evidence the deficit is too small. Either way, the deficit does matter.

As far as “printing money” is concerned – it is worth noting when the Government spends, it effectively prints money, which becomes the source of private sector savings. When it taxes, it “un-prints”. Australia has been a serial money printer over the past 120 years, and especially over the past six years. Low unemployment and rising inflation are not considered a problem in today’s environment.

Does Australia’s sovereign credit rating matter?

In a word, no.

Businesses and households can go broke. This is because they are currency users. The Australian Government, in conjunction with the RBA, is a currency issuer. A currency issuer can always pay its bills so long as those bills are denominated in the currency of issue.

Of course the Government can choose to default on its obligations. For example, the existence of a debt ceiling is a political constraint to ongoing deficits. But this self-imposed constraint is easily altered by way of a parliamentary vote.

How does this insight fit with Quay’s investment process?

At Quay, along with our deep understanding of real estate, we have spent nearly 10 years researching and understanding the mechanics of the monetary system, both here and overseas. We think this understanding gives us a powerful edge to invest globally.

For example, there is much debate in the United States about the “affordability” of healthcare and unfunded future Government liabilities. These sentiments can weigh on the value of healthcare assets – as it has done recently.

However, so long as US healthcare bills are denominated in US dollars, the Government can always “fund” healthcare costs – forever. Funding health care is a political choice – not an economic choice. The real constraint is not dollars but the physical resources required to service the aging population. The Government can issue USD – but it cannot “issue” a doctor, nurse or hospital.

Therefore, as long-term investors it makes sense to look beyond the noise of ratings agencies and politics by focussing on the underlying issues. Gaining exposure to desirable assets that are constrained with secular demand tailwinds. Understanding what matters – and what doesn’t – is critical to our approach.

Appendix A –deficit spending by the Australian Government

Background

The spending arm of the Australian Government is the Treasury. The Treasury’s bank is the Reserve Bank of Australia (RBA). The Treasury’s cash balance is recorded as a liability on the RBA’s balance sheet, in the same way as a household deposit is recorded as a liability at a commercial bank.

The RBA is also the bank for all of our banking institutions. Banks hold cash at the RBA known as exchange settlement balances. These balances also are recorded as a liability on the RBA’s balance sheet.

One of the RBA’s primary roles is to act as a clearing house for the banking system. When households and businesses transact with each other, the commercial banks move their cash balances at the RBA to settle the transaction.

For example, when an individual buys a $500 TV from a retailer, that person’s bank (e.g. NAB) will transfer its cash balance at the RBA to the retailer’s bank (e.g. CBA). At the same time, the individual’s deposit balance will fall by $500, and the retailer’s deposit will increase by $500. The NAB will have $500 less in deposits and cash at the RBA, while CBA will have $500 more in deposits and cash at the RBA.

Understanding this process is critical before we move to the function of government spending.

How the Central Bank (RBA) control interest rates

Most people will know the RBA sets the cash rate. But many probably do not understand how this is achieved. It is critical to understand this process so as to fully follow the mechanics of government spending.

According to the RBA website:

“As part of its responsibility for monetary policy, the Reserve Bank Board sets a target for the cash rate. This is the rate at which banks borrow from and lend to each other on an overnight, unsecured basis. The rate is determined by the demand and supply of exchange settlement balances that commercial banks hold at the Reserve Bank. Through its open market operations, the Reserve Bank alters the volume of these balances so as to keep the cash rate as close as possible to its target.[8]” (Note: Emphasis made via the above bolded text is the author’s.)

So the RBA manages the amount of cash (exchange settlement balances) to achieve a target rate. The RBA achieves this by paying banks a return on the excess cash held at the RBA – but it is 0.25% below the target rate (currently 1.50%). Banks can also use standby facilities to access cash by borrowing from the RBA, on a secured basis, 0.25% above the cash rate (currently 2.00%). This +/-25 basis point “collar” encourages banks with excess cash balances to lend to banks with a deficiency. In a normal market, the interbank rate settles at the mid-point – currently 1.75%.

In our earlier example, the amount of cash (exchange settlement balances) held by the commercial banks has not changed. But NAB is short of cash, and CBA has excess. The CBA is encouraged to lend $500 to NAB at the target rate.

When the RBA changes the interest rate, they move the collar up (or down) so the mid-point moves to the new target rate.

The mechanics of government spending

When the Government approves spending, the Treasury is directed to make the appropriate payments to the private sector. That may be to households, businesses, States, etc.

Payments are made by directing the relevant banks to mark-up the deposit accounts of the recipients of government spending. To settle the transaction, the Treasury transfers its cash balance at the RBA to the relevant banks.

So commercial banks’ cash balance at the RBA (an asset) increases in recognition of the new household/business deposits.

However, this higher cash level held by the banks attracts a lower rate of interest compared to the interbank rate (1.50%) and that is generally not enough to cover the interest payable on their new customer deposits (~1.75%). So to maximise interest on cash, the banks try to lend to each other in the inter-bank market at the target rate of 1.75%. However, the effect of government spending has tipped the cash balance of the financial system such that there are too many lenders and not enough borrowers. If left unchecked, the interbank rate will fall to the lower level of 1.50%, and the RBA will lose control of monetary policy. At this point, the RBA intervenes with open market operations.

RBA open market operations

To return the inter-bank market back to the target rate, the RBA must intervene by way of its open market operations. As the RBA states:

“Securities transactions are conducted almost every day in the ‘open market’ by the Reserve Bank. Each morning, the Reserve Bank announces its dealing intentions, inviting financial institutions to propose transactions that suit the Reserve Bank's purposes. Counterparties are able to sell highly rated debt securities to the Reserve Bank either under repurchase agreement (repo) or outright sale.”

So when the banks have too much cash, the RBA intervenes and allows the banks to buy securities from the RBA (known as repurchase agreements or repos). This reduces the bank’s cash balances at the RBA and provides the banks with a better interest rate. The cash in the system returns to its previous level, and the interbank cash rate remains at 1.75%.

What qualifies as a "repo"?

The RBA provides a list of “eligible securities” on its website, as shown below. Please note we have formatted government securities in red to highlight the fact that these securities are eligible irrespective of the credit ratings.

This ensures there is constant demand for Australian government bonds, since they will always qualify as a source of liquidity with the RBA, no matter what the ratings agencies say. The fact bonds usually pay more in interest compared to exchange settlement balances adds to the appeal.

|

|

|

Minimum S&P Credit Rating (or Moody's / Fitch equivalent) |

|

Australian Government Securities |

n/a |

|

|

Semi-Government Securities |

n/a |

|

|

Foreign Government securities |

AAA |

|

|

Securities with Australian Government Guarantee |

n/a |

|

|

Securities with Foreign Government Guarantee |

AAA |

|

|

ADI Issued Securities |

||

|

- Residual Maturity greater than 1 year |

BBB+ |

|

|

- Residual Maturity greater of 1 year or less |

Public Credit rating |

|

|

Asset Backed Securities |

A-1 or AAA |

|

|

Other securities |

a-1 or AAA |

|

Source: RBA website

The Treasury can run out of money – but the rules around bond issuance stack the cards in favour of the Government

The Australian Treasury is generally not allowed to run an overdraft with the RBA[9]. After it depletes its cash balance from net spending, it is required to raise funds via bond issuance to the extent tax receipts fall short. The Australian Office of Financial Management (AOFM) issues new bonds.

Banks and other qualified buyers bid for the new securities via the “yield method”. The allocation of bonds is determined by price.

Why do banks (and their customers) bid for the bonds?

- Firstly, after the Government spends, the banks have too much cash and incur a penalty interest rate – so buying a government bond reduces the cash held and gives the banks a better return

- Note, if a bank customer buys the bond, the bank will settle the transaction by transferring its cash to the Treasury. It therefore has the same effect of draining the excess cash from the system as if the bank bought the bond directly

- The banks understand the bonds are as good as cash since they are an “Eligible Security” under the RBA Repo facility and can be used to gain liquidity at any time, irrespective of the credit rating

- However if the banks cash needs are in balance, the RBA will conduct open market operations to ensure the banks have the cash to acquire the bonds. Not because the RBA seeks to finance the Government, but because the RBA is focused on maintaining a target cash rate

After the newly issued bond is sold, the Treasury has restored its cash balance and the whole process can start again.

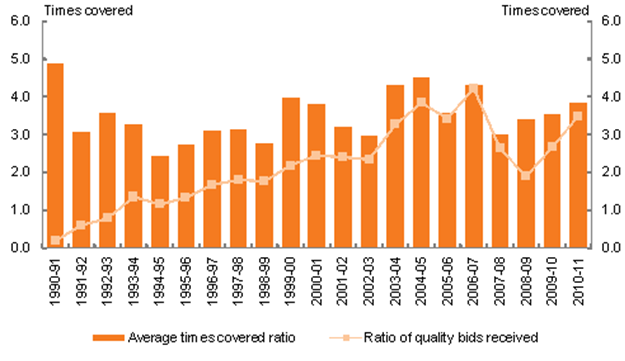

The process is repeatable because the Government spending creates the funds to buy the bonds. Upon settlement, the cash is returned to the Treasury in exchange for a bond so the central bank can maintain its target interbank rate. As a result of this process, the AOFM has never had a problem attracting enough bids for its bond auctions – either when the country was running surpluses (1998-2007) or deficits (2009-2011, 1990-1997). Also note Australia’s credit rating in 1990 was two notches below the current rating a when the bid cover ratio was at its highest. See historic bid cover ratios below (number of dollars bids per dollar of bond offered).

Source: Australian Office of Financial Management

Summary

Under Australia’s current financial structure, the Australian Government will always get the funding it needs. This is because:

- when the Government net spends, the banks (and customers) receive excess cash which, if left

unchecked, will drive down interest rates (by 25 basis points) and hurt bank profitability; - after the spending, the banks are always willing buyers of government backed securities to avoid the 0.25% penalty. The RBA assists with open market operations since the RBA is targeting an interbank interest rate;

- banks and other sophisticated investors know government bonds are as good as cash (with a better return) since they qualify as an “Eligible Security” irrespective of the credit rating; and

- this means there is no default risk to government bonds outside of normal political constraints (such as maintaining an artificial debt ceiling).

Of course this is the technical process. But if that was a bit hard to follow, common sense will tell you the credit rating of Australia does not affect the Government’s ability to pay its bills, so long as those bills are denominated in Australian dollars.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.

[1] http://www.theguardian.com/business/2016/apr/14/australia-cant-balance-budget-with-spending-cuts-alone-says-moodys

[2] Although commercial banks create money via the loan process, banks must support their expanded balance sheets with increasing levels of Exchange Settlement Accounts (cash at the RBA), which in turn are supplied by the RBA.

[3] Source: AOFM website; http://aofm.gov.au/statistics/historical-data/commonwealth-government-securities-on-issue/

[4] Source: AOFM website; http://aofm.gov.au/statistics/non-resident-holdings/

[6] http://www.bloomberg.com/news/articles/2016-01-10/china-retreat-from-u-s-bonds-prompts-shrugs-where-fear-reigned

[7] It is possible for the Household sector and the Government to run surpluses simultaneously, however it relies on one or both of the remaining sectors (foreign and business) to run a financial deficit.

[8] Source: RBA Website: http://www.rba.gov.au/mkt-operations/

[9] The Reserve Bank provides an overdraft facility for the Government that is used to cover periods when an unexpectedly large mismatch exhausts cash balances. The agreement between the Treasury and the Reserve Bank places strict controls on access to the overdraft facility, as well as imposing a market-related interest rate on the facility. The overdraft is used infrequently, generally to cover unforeseen shortfalls in cash balances, and is extinguished at the next Treasury Note tender.