Global listed infrastructure is set for continued strong growth to 2020 and beyond. This is due to a combination of powerful global forces driving a need for increased infrastructure investment, namely:

- a chronic under spend on critical infrastructure over the past 30 years - in virtually every nation;

- the emerging middle class, especially in developing economies, continues to demand more and better infrastructure; and

- public sector fiscal positions remain fragile, thereby limiting the potential fiscal response available to governments.

1. Under investment in infrastructure has been chronic over the past 30 years

The lack of public investment in infrastructure over the past 30 years has been a feature in both developed and emerging economies. This has been a well chronicled trend.

- The 2015 Infrastructure Australia Audit Report highlighted that without a total increase in both public and private funding of infrastructure, Australia won’t have the infrastructure that a growing population and a globally-focussed economy deserve.

- The 2011 OECD Report, Strategic Transport Infrastructure Needs to 2030, estimates US$53 trillion of infrastructure investment is needed by 2030 to meet the demand over coming decades, with US$11 trillion of that needed for ports, airports and key rail routes alone.

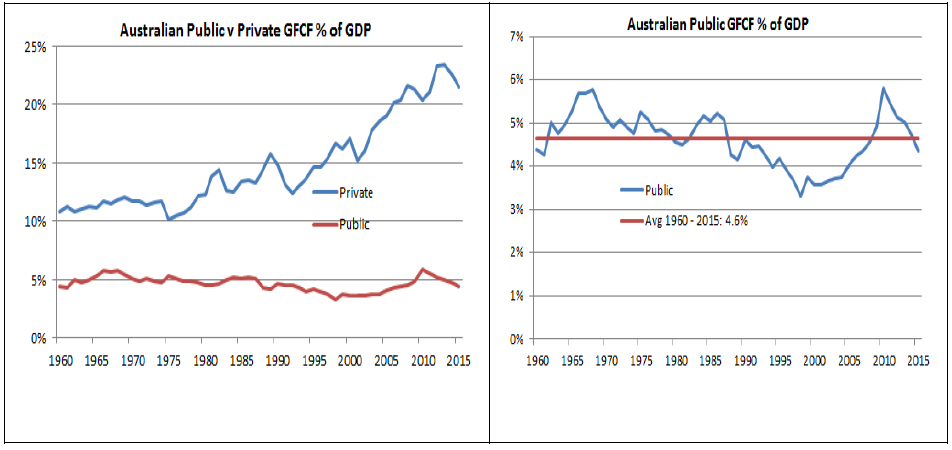

The findings above are consistent with the Australian experience. The charts below show Public and Private Gross Fixed Capital Formation (GFCF) in Australia from 1960. While GFCF is a broader measure than just infrastructure investment, the patterns evident provide an insight.

The average Public GFCF/GDP (%) from 1960 has been ~4.6% pa (Chart 1 on the right hand side below). However, this masks a significant and extended dip below this average from around 1985, a brief recovery in 2009-10, and the ratio trending sharply lower since. It has averaged only ~4.3% pa over the past 30 years, consistent with the general deterioration in the national infrastructure stock that has occurred during that time.

Chart 1: Australian GFCF from 1960

Source: Australian Bureau of Statistics

2. Emerging markets and the new middle class: better/more infrastructure needed

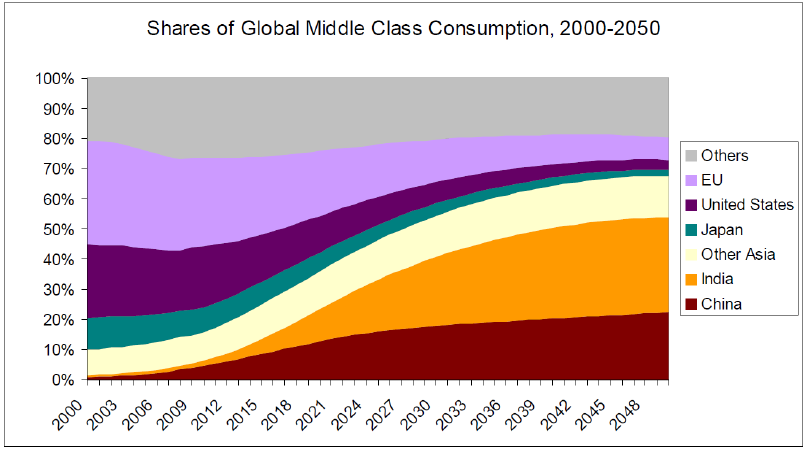

Emerging markets are in the midst of one of the most powerful and enduring themes that the global economy will experience over the next 50 years – the emergence of a middle class. As shown in Chart 2 below:

- in 2000, Asia (excluding Japan) accounted for 10% of global middle class spending; and

- by 2030 this could reach as high as 40%, and move beyond 60% longer term.

Chart 2: Shares of Middle Class Consumption, 2000-2050

Source: 2010 OECD Development Working Paper 285

A growing middle class inevitably demands more and better infrastructure to service and support their improving living standards. Privately funded infrastructure will continue to be a growing source of funding to meet that demand.

3. Fiscal positions remain fragile limiting the potential government response

Historically, infrastructure investment has been the domain of the public sector. However, this is gradually changing and is set to accelerate because of the fragile state of public sector finances around the world.

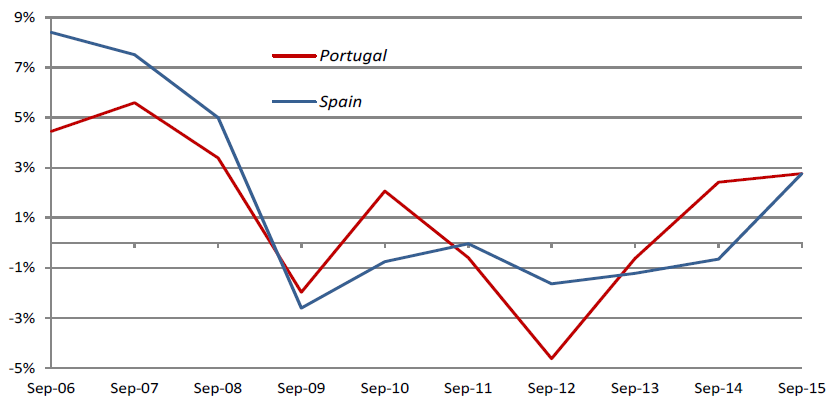

This point is illustrated through the fiscal positions of two countries that were prominent in the GFC: Spain and Portugal. As shown in Chart 3 below, both Spain and Portugal are making solid post-GFC recoveries as measured by GDP growth. While both countries suffered severe and protracted GFC induced recessions, including a period of tough austerity measures, each country’s growth profile is now back in positive territory.

Chart 3: Spain vs Portugal GDP growth

Source: Bloomberg

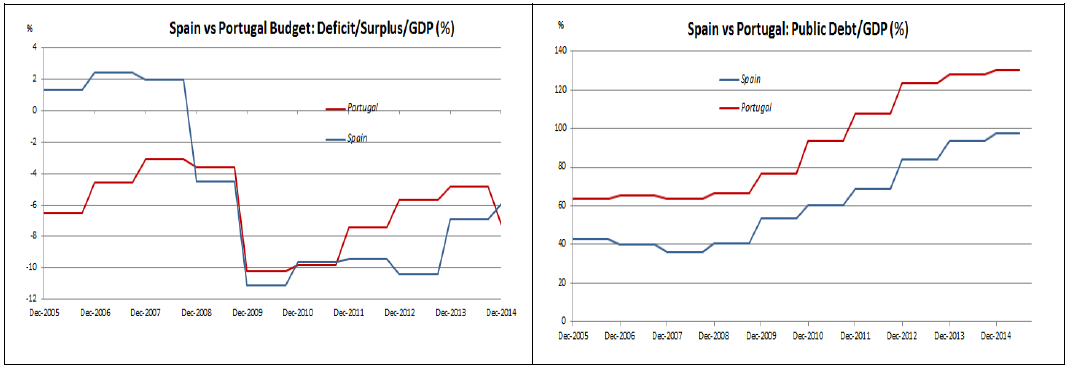

However, while GDP growth has returned, a residual GFC hangover is evident in Chart 4 below. Both countries’ Budget Deficits have contracted somewhat, but Public Debt/GDP (%) has continued to rise.

Chart 4: Spain vs Portugal economic profile

Source: Bloomberg

Spain and Portugal are not unique with this post-GFC economic profile of recovering GDP growth, persistent fiscal deficits and high/expanding public debt/GDP ratios. Canada, for example, has public debt/GDP of 95%, the US 75%, France 96%, Japan 232% and Italy 132%.

Fragile fiscal positions will compel greater private sector involvement

The implications for potential infrastructure spend are clear – fragile fiscal and balance sheet positions will constrain public sector infrastructure investment over the medium term. By necessity and opportunity, the private sector will need to play an increasing role going forward.

Conclusion

There has been substantial under investment in the global infrastructure stock over the past three decades. Combined with the emergence of a growing middle class, especially in Asia, means there is a growing need for increased infrastructure investment around the world. However, government fiscal positions remain fragile post-GFC. As a result their ability to fund the necessary investment is constrained, and increased private sector involvement in funding the capital demands will be a necessity.