While the sums involved are not great, the real value is gained by reminding myself of an important human trait - recency bias. The tendency to think that trends and patterns we observe in the recent past will continue in the future.

The betting strategy works (on average) because markets are set by people. And people have a hard time ignoring recent history when thinking about the future. Yet in the NRL, teams lose and gain players, coaches and sponsors between seasons. The salary cap is designed to rebalance the competition each year (mean revert). Yet the odds for the first round every year generally reflect the prior year’s performance. There exists a disconnect between price and probability.

Recently, there has been much discussion regarding the prospects for Australian residential property. From high profile media coverage predicting a ‘mortgage meltdown’ to debate in parliament suggesting changes to negative gearing will trigger an Australian property price collapse.

Indeed, type ‘Australian Property Bubble’ into Google and the search will return no less than 500,000 results.

So, is it a bubble or does this simply reflect the recency bias of the GFC?

At Quay, we try to avoid such emotive terms. We also prefer not to think about fair value but rather prospective returns. The Japanese Real Estate Investment Trust (J-REIT) for example may be fair value, but their prospective returns are low. In this respect we feel the prospective return prospects for Australian property to be quite low on a medium term to long-term basis.

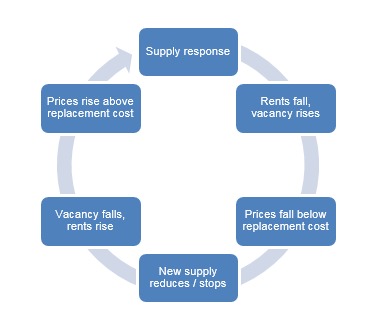

Regular readers may recall Quay’s framework when assessing property cycles. We consider most property to be ‘commodity’ in nature. That is, it is easily substituted or replaced when the development profit equation favours new supply. We consider most residential property to be commodity in nature, especially when credit is widely available. Below is a diagram depicting our view on the cycle for typical commodity property.

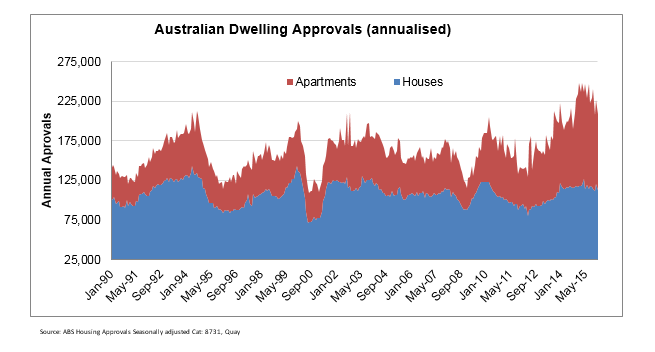

From an Australian residential property perspective, it seems we are at or around the ‘supply response’ stage. The following approvals chart from the ABS confirms this view.

Some may argue that Australia has experienced a housing shortage in previous years, and that may be true. However, that does not alter the reality that Australian house prices, on average, are trading well above the cost to build (including land), which has facilitated a strong supply response. In fact, as per the chart above, dwelling approvals are running at a record pace.

When prices are greater than the cost to produce, it is unlikely prices will continue to grow at or above inflation – since that will only stimulate more supply which is unsustainable. It is more likely prices will grow at a lesser rate than cost. That is, real prices will fall, leaving investors to rely on yield to make up most of the total real return.

So how do Australian property yields stack up?

Comparing yields on a like-for-like basis

‘Yield’ can be quoted three different ways for the same property:

- Gross Yield;

- Net Yield = Gross yield minus operational expense (rates, leasing costs, marketing, etc.); or

- Free cash flow yield = Net Yield minus recurring capital expenditure (building structure, internal fixtures and fittings, carpet, etc.).

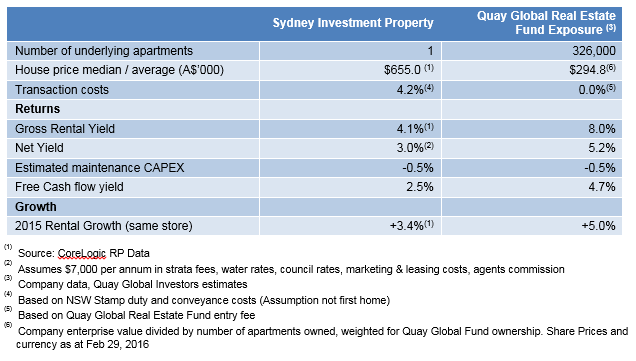

In Australia, residential investment yields are generally quoted on a gross basis. For a typical apartment in Sydney, the average gross yield is around 4.1%, which looks ok compared to cash and bonds.

But what is the true free cash flow yield and how does it compare to global benchmarks?

We can compare the investment metrics of a typical Sydney apartment to the metrics of the apartment exposures we have in the Quay Global Real Estate Fund. The table below compares gross yield, net yields and free cash flow, as well as historic rental growth and transaction costs.

In summary, when compared to Quay’s Global apartment exposure, Sydney apartments have:

- lower gross yield (in a higher interest rate environment);

- lower net yield;

- lower free cash flow yield;

- higher transaction costs; and

- lower historic growth.

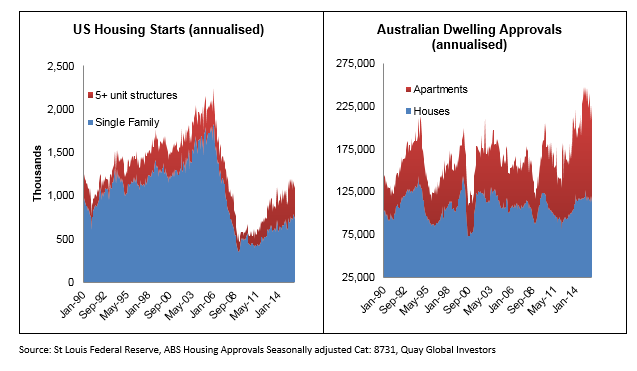

On average we expect our investees to deliver 4.9% rental growth in 2016. In Sydney, there is no consensus on rental growth for this year, however, when we look at new supply compared to (say) the US, it is difficult to mount an argument that it will be much better than last year.

Concluding thoughts

Recency bias is a powerful human trait that has been instrumental to human survival. For instance, when we touch fire it burns, so we learn not to do it again. But in the ever changing world of investment where prices and fundamentals are always changing (much like NRL teams), it is a trait that could result in missed opportunities or unintended risk.

This may be occurring regarding commentary around Australian real estate today as the scars from the GFC are still raw. Without buying the “is it/isn’t it a bubble” argument, at Quay we simply look at the best return prospects. And based on the limited supply outlook, yield and growth profile, we continue to remain comfortable with our international apartment exposure.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.