1. Government privatisations: a key part of the asset ownership transition process

In Part 1, we examined the fragile fiscal positions facing governments around the world, and why that will inhibit their ability to fund much needed infrastructure capex. Privatisation of public assets is one of the options cash strapped governments will turn to in confronting revenue pressures. It is also an important part of the public/private ownership transition mechanism that will lead to growth in listed infrastructure over the coming decades.

To illustrate this in practice we look at two current privatisation programs.

-

NSW electricity asset privatisations: long-term leases

In June 2014 the NSW State Government announced that it intended to privatise the NSW electricity networks comprising: TransGrid(a transmission business with a regulated asset base (RAB) of A$6.1 billion), AusGrid (a distribution business supplying 1.6 million customers, with a RAB of A$14.6 billion) and Endeavour Energy (a distribution business with 883,000 customers, and a RAB of A$5.6 billion) (Norton Rose, July 2014).

The Liberal Party successfully took this privatisation policy to the March 2015 NSW state election. In June 2015 the NSW parliament passed the enabling legislation for the privatisations. The State Government plans to lease, for 99 years, 100% of Transgrid, and 50.4% of Ausgrid and Endeavour, and it hopes to raise $20 billion from the privatisations to spend on road, rail and other infrastructure projects. (SMH, 4 June 2015)

While the major purchasers of these assets will likely be superannuation and/or unlisted infrastructure funds, some of the equity will find its way to the public market, either at the time of purchase or over the longer-term. So far, in NSW the lease of the transmission business TransGrid has been announced, with a value of A$10.3 billion.

The winning NSW Electricity Networks consortium included the ASX listed Spark Infrastructure (SKI). SKI will hold 15% of the equity (for an investment of A$734m), and is partially funding this holding via a A$405m equity entitlement offer to existing shareholders. (SKI, Retail Entitlement Offer Booklet, November 2015)

The NSW experience illustrates how privatisations can lead to an expanded role for private sector finance, including the listed equity markets, in the infrastructure funding mix. It also shows how governments, faced with fiscal pressures but recognising the need for infrastructure capex, are willing to adopt forward thinking policies as a means of delivering on those objectives.

-

US water and waste water sector: privatisation program

Another privatisation program, in a very different form, is underway in the US water and waste-water (sewerage) sector. This industry is not only in need of substantial investment (for example, the US EPA estimates a capital investment program of US$633 billion is required over the next two decades to maintain and improve water and waste water facilities in the US) but is also extremely fragmented.

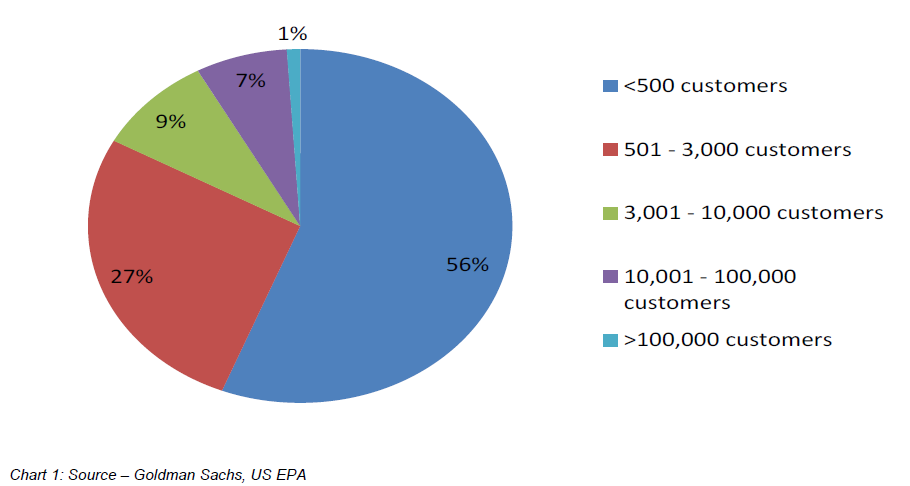

As shown in Chart 1 below, there are over 53,000 water systems in the US today, serving 300 million Americans. However, only 8% of the country’s systems serve populations of over 10,000, and a mere 1% of systems serve over 100,000 customers. This is a sector in need of consolidation.

Chart 1: Distribution of US water service provider by number of customers (% of total)

Many small local US water municipalities are facing significant challenges to replace ageing water infrastructure and spread the cost across small customer bases. Facing material customer bill increases, many public municipalities seek alternative solutions such as selling their asset/customer base to major, listed US water utility companies. These so called ‘tuck-in’ acquisitions are very attractive for the big listed US utilities. They are able to acquire new customers/assets at attractive prices, while substantially absorbing the costs associated with the acquisitions within their existing overhead base.

The US water experience illustrates both how privatisations can lead to an expanded role for public companies in the funding of infrastructure, as well how larger, more efficient private sector utilities can deliver essential services on a more cost effective basis.

2. Why will listed infrastructure perform an increasing role in the funding solution?

We believe the case for much needed global infrastructure investment to be increasingly funded via the public equity markets around the world is compelling. This is because the fundamental characteristics infrastructure assets offer are ideal for public market participation.

Key features of global listed infrastructure (GLI) assets include:

- long dated, resilient and visible cash flows;

- regulated or contracted earnings stream(s);

- monopolistic market position, or one with high barriers to entry;

- attractive potential yield;

- inflation hedge within the business;

- low maintenance capital spend;

- largely fixed operating cost base; and

- low volatility of earnings.

Translated to public equity markets, these characteristics deliver companies with clear growth profiles, predictable, resilient and transparent earnings together with attractive dividend yields.

Over the past decade GLI portfolios of assets with these characteristics have delivered strong market performance across all cycles, lower volatility of returns and a strong dividend yield as illustrated in the following charts.

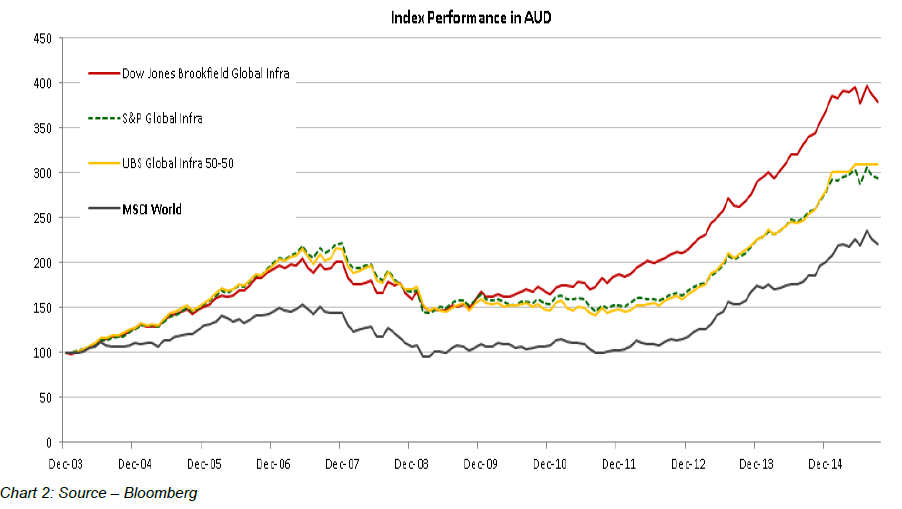

GLI has outperformed broader equities since 2004

Since 2004 (when GLI became more accepted as a separate asset class) the three major GLI indices have all outperformed the broader MSCI World index, as shown in Chart 2 below.

Chart 2: Performance of three GLI indices v the MSCI World index (from January 2004)

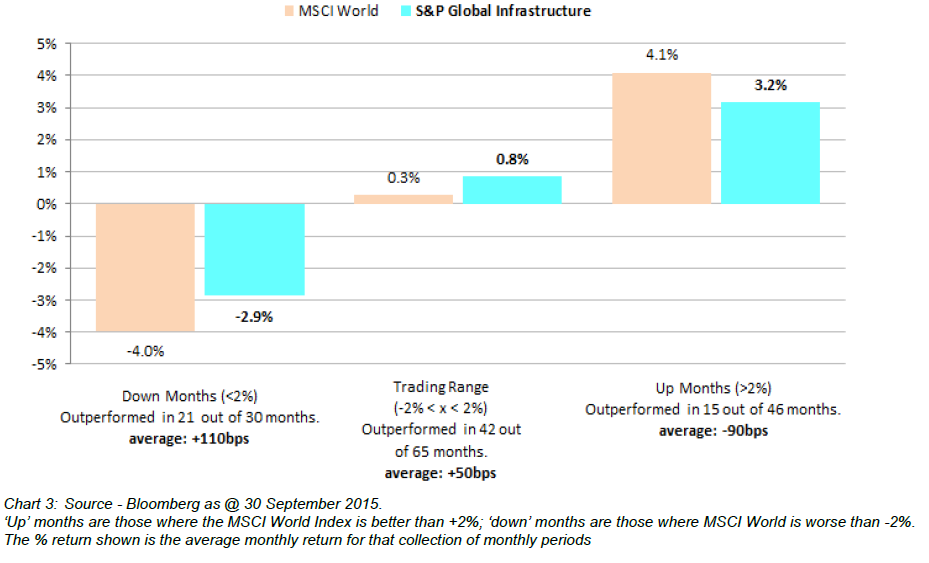

GLI has outperformed during the tough market months

An important feature of the GLI performance shown above is that it has been strong during the tough market months – when the broader market was flat or down. As shown in Chart 3 below, since January 2004:

- during the 30 MSCI World Index (MSCI World) ‘down’ months GLI (as represented by the S&P Global Infrastructure Index (S&P Infra Index)) out-performed the MSCI in 21 of those months;

- during the 65 MSCI World ‘flat’ months the S&P Infra Index out-performed the MSCI in 42; and

- only during the 46 MSCI World ‘up’ months did the S&P Infra Index slightly under-perform the MSCI World – beating it in 15 of those 46 months.

Overall, from January 2004 to September 2015, the S&P Infra Index out-performed the MSCI World in 78 of 141 months (55%), delivering an average monthly outperformance of 17bp.

Chart 3: Performance of the S&P Global Infrastructure Index v MSCI World Index

(from January 2004, characterised by type of monthly market performance)

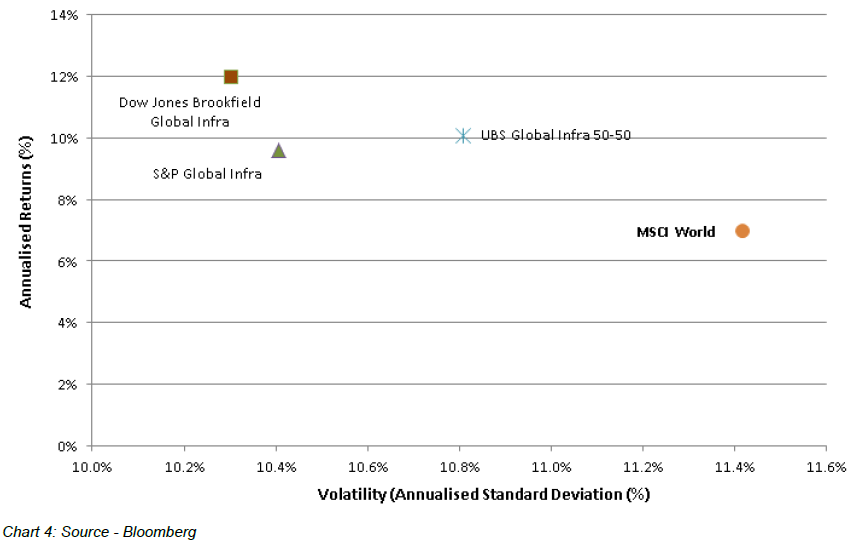

GLI delivers its returns with lower volatility

A further important feature of the performance of GLI is that returns have been accompanied by lower volatility as compared with the broader equity market, as shown in Chart 4 below.

Chart 4: Three GLI Indices & the MSCI World: Volatility v Return (from January 2004)

GLI provides strong, stable dividend flows

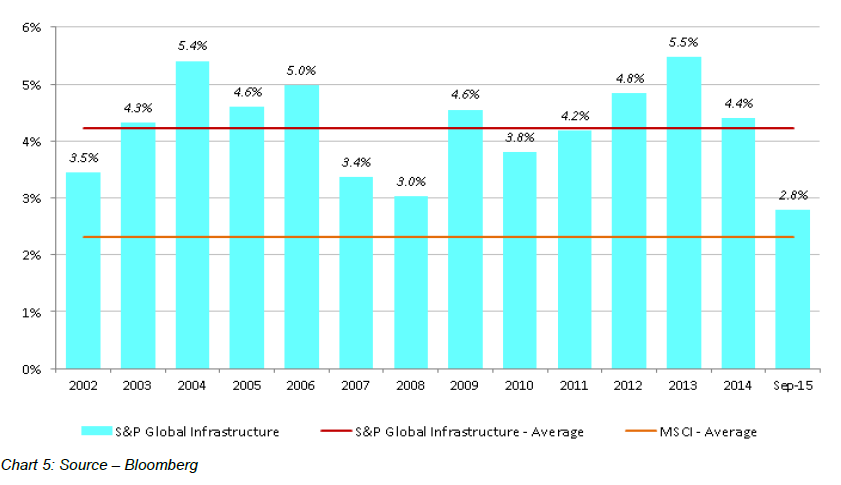

Finally the quality of earnings available from GLI stocks facilitates higher dividend yields as shown in Chart 5 below.

Chart 5: S&P Global Infrastructure Index Dividend Yield v MSCI World average

GLI: a valuable addition to equity portfolios

GLI’s strong historic performance, its capacity to out-perform in tough markets, with lower volatility of returns and strong dividends makes it, in our view, an asset class that is a valuable addition to all equity portfolios.

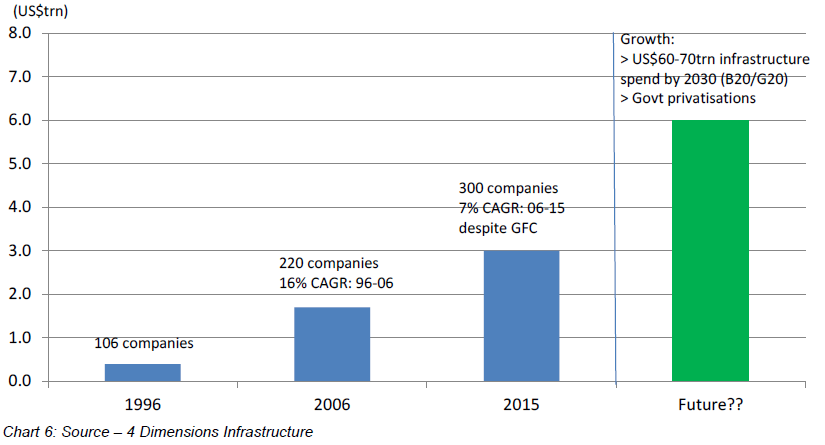

As shown in Chart 6 below, the GLI market capitalisation in 2006 was ~US$1.7 trillion with 220 companies. It is now ~US3 trillion, with around 300 companies. We believe this rapid growth trend will continue over the next 10 years.

Chart 6: Growth in GLI Market Capitalisation

Conclusion

Government fiscal positions remain fragile post the GFC, constraining their ability to fund necessary investment in often long neglected infrastructure. Privatisation of public assets is an important transition mechanism for increasing GLI’s share of the infrastructure funding mix. What’s more, the attractiveness of the sector to investors – evidenced by a strong historic performance – makes it well placed to continue on its growth trajectory, as it serves an increasing role in the worldwide solution to funding an ever expanding infrastructure need.