What struck us was how often the conversation turned to direct market transactions and how this translated to the company’s NAV per share (unlike Australia, US REITs do not revalue assets, so book NTA’s are largely meaningless).

Summary

- Net Asset Value (NAV) investing implicitly relies on the assumptions and return objectives of third party investors or assessors

- NAV investing potentially encourages pro-cyclical investment decisions

- Investing in listed real estate on the basis of NAV can miss crucial elements of total return

- Poor pay-out ratios, balance sheets or a limited investment opportunity set may result in companies trading in line with NAVs over time, but still generating unacceptable total returns

- At Quay, we challenge the status quo to standardised valuation and offer a different approach to identifying returns – and we believe this gives us an edge.

NAV investing remains popular across the industry

While in New York recently at a global real estate conference, we attended a number of company meetings with other participants. What struck us was how often the conversation turned to direct market transactions and how this translated to the company’s NAV per share (unlike Australia, US REITs do not revalue assets, so book NTA’s are largely meaningless).

And an interesting observation while attending another recent real estate conference, this time is Australia, was gained from a panel of CEO’s representing some of the largest REITs in Australia across office and retail sectors. It was remarked that in the currently environment prime office cap rates in Sydney are firmer than regional mall cap rates. Intuitively, this doesn’t make sense given higher levels of capital incentives and risk of substitution.

At Quay, we find these transactions interesting but irrelevant to our investment process because:

- the transaction metrics of a direct property sale reflect another party’s expected total return which could be different to our benchmark;

- direct property investors can be just as irrational as listed investors; and

- as long-term investors we focus on free available cash flow to shareholders. Changes to NAV may reflect changes in cash flow, but do not influence cash flow.

Investing for total return, not relative return

Clearly, there is an argument to use direct market truncations to justify higher listed property prices. In a world of relative investing this may make sense. We always feel good if our neighbour paid 10% more for their house.

But when investing with an ‘absolute return’ focus, this type of information alone is not enough to give us comfort in forming a view on value. The more important question is, have I overpaid for my house?

Thinking about total return in real estate, we turn our minds to the free or after maintenance capex cash flow to equity investors. It is this approach that allows us to disregard historic valuation norms (cap rates) when identifying investment opportunities. We do this by beginning with our assessment of a fair capitalisation rate for each asset class.

We also think about pay-out ratios and the ability (or willingness) for businesses to re-invest in additional assets or improve existing assets. The relative investment opportunity set is critical in this regard. This is an important component of total return that is often overlooked by NAV style investment.

Thinking about a fair cap rate

When investing for a total return, we remove ourselves from comparable sales and think purely about the prospects of each investment. That way, we can more easily benchmark between Office, Health and Mall assets because we value each asset type on a like-for-like basis by using our fair cap rate approach.

Quay’s construct of a fair cap rate across each asset class is a proprietary approach based on:

- our minimum long-term real return requirement;

- benchmarking operational CAPEX;

- benchmarking long-term real rental growth; and

- trend cash flows rather than one-year forward income.

When constructing fair cap rates, we derive very different answers compared to historic cap rates. For example, we see no theoretical reason why Midtown New York Office or London Office property should have a lower cap rate than, say, Bunnings Warehouse Property Trust.

Of course, in the direct and listed world there is a huge difference between market accepted cap rates and our approach, and therein lies the opportunity.

We read a number of sell side reports and they do an outstanding job of assessing a REIT’s prospects and near-term cash flows. Over 95% of the analysts’ work is dedicated to the near-term financial forecasts. Their assessed NAV applies a cap rate to the forecasts. The applied cap rate, which determines the value, seems to attract only 0-5% of the thought process and usually reflects the most recent direct/indirect sales evidence.

This approach results in a highly pro-cyclical approach to value. Higher prices (lower cap rates) feed back into analyst models and expectations of higher NAVs. The result is higher cyclical highs and lower lows as the cycle unwinds.

By remaining focused on the appropriate cap rate for a target total return (and ignoring the market noise), we believe our process will assist avoiding the worst of the cycle.

Plough-back and the relative opportunity set

Net Present Value (NPV) investing is different to NAV in that it takes free cash flow and assumes an investor required total return (discount rate) to arrive at a fair value.

This approach is better than NAV as it recognises the importance of free cash flow but gives little thought to pay-out ratio, marginal return on capital and relative opportunity set.

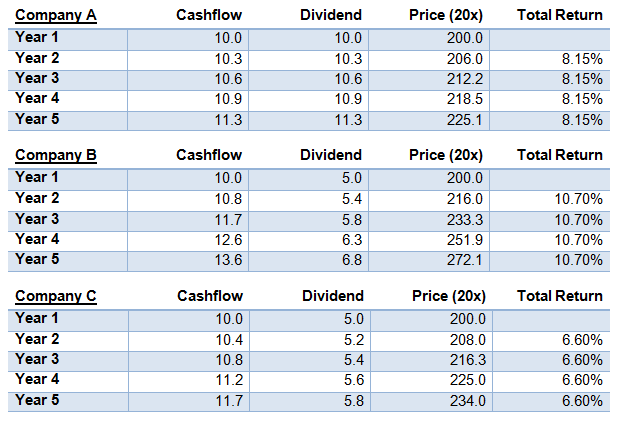

Consider three companies all in the REIT universe. These companies have the following characteristics:

- Company A earns $10 p.a. after maintenance CAPEX and distributes $10 p.a. It’s marginal return on equity is 10% p.a.;

- Company B earns $10 p.a. after maintenance CAPEX and distributes 50% of income ($5 p.a.). It’s marginal return on equity is 10% p.a.; and

- Company C earns $10 p.a. after maintenance CAPEX and distributes 50% of income ($5 p.a.). Its marginal return on equity is 2% p.a.

Each company has the same underlying cash flow growth of 3% p.a., the same balance sheet and the same quality assets.

How does each investment approach (NAV, NPV and Total Return) assess each investment option?

The ‘NAV investor’ will have the same value for each company, as they would apply the same multiple to the $10 cash flow (same cap rate to the un-levered cash flow).

The ‘NPV investor’ will have very similar results for each company because implicit in the discount rate is the same marginal return on capital for every company.

The ‘Total Return Investor’ will value company B the highest because this business will increase the value of assets over time.

To understand this better, the table below traces the total annual return of each company over time assuming a static 20x earnings multiple (5% equity yield). The total return is the change in annual price plus the dividend yield.

Company B delivers the best total return because:

- while it pays a low dividend compared to company A, it is growing its dividend and cash flows at a greater rate;

- relative to company A, the additional growth rate (5%) is greater than the lower yield (2.5%) because it is re-investing the retained cash flow; and

- relative to company C, company B offers the same yield but is growing cash flows at a greater rate because it is re-investing at a higher return.

Investment implications

There are a number of implications of investing for total return rather than relative return.

- We think about cap rates from a total return perspective – not based on historic norms. This creates a very different set of investment ideas compared to an investor who assesses NAVs using historic precedents.

- Pay-out ratio is important. While many REIT’s are required to distribute 90-100% of taxable income, in many instances the actual number is well below 90-100% of free cash flow. Indeed, some of our largest investment positions have pay-out ratios of 50% to free cash flow, which drives total return.

On the other-hand many other REITs however, distribute far in excess of 100% of free cash flow, and many do this when they have a requirement or opportunity to re-invest. This creates a cycle of higher gearing or a reliance on fresh equity and lower long term equity returns. These entities we shy away from.

- But low pay-out ratios in isolation are not always a good thing. The marginal return on capital is equally an important driver of total return.

It is worth noting company A could have very attractive total return so long as it issued new equity at a price which reflects a low total return (i.e. at a premium). The model works so long as the share price allows it to work. CEOs of this type of company often talk about their ‘cost of equity’ as an important driver of their business. Since we like companies with a high total return (or cost of equity), we find it difficult to mount a strong investment case for these businesses.

Regular readers will know our portfolio is well weighted to sectors like Storage and Health. These companies have very low ‘stay in business CAPEX’ requirements, which means that free cash flow available to shareholders is relatively high. As these companies also retain free cash after dividends, there is the opportunity to grow cash flows without relying on shareholders. Further, according to most industry estimates, the public REITs in these sectors only own ~15% of total assets in these sectors. Therefore the opportunity set is huge. A similar story can be made for Student Housing where campus re-generation could last for decades.

Conclusion

At Quay we understand there is no one way to invest. Each approach has its merits and limitations. NAV investing has its place – especially for investors focusing on relative returns. However, Quay’s approach is to focus on total after inflation or real returns. We gain no satisfaction in beating an index only to lose a client money when the cycle turns. Our focus is therefore different – leading to different opportunities and over time, acceptable total returns while minimising the risk of permanent capital loss.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.