The total value of listed equities in Australia is estimated to be $1.5 trillion. Government bonds $0.4 trillion. Real estate is more than three times these asset classes combined at approximately $7 trillion.

These ratios are not dissimilar to other developed markets. If an investment portfolio were to be weighted by relative size (like most equity indices), real estate would, by far and away, be the single largest exposure for most people. And for many it is - the family home.

However, as people accumulate wealth in life, they tend to diversify away from real estate into other holdings. This can make sense, however, as the oldest form of investment, land has proven to be a spectacular way to preserve and build wealth over generations. We believe there is a case for real estate to remain the cornerstone of any wealth preservation and accumulating strategy.

A sector hard to ignore

The financial crisis of 2007-2009 gave real estate a bad name. Sold as a “proxy for bonds” (it isn’t), investors were understandably dismayed their low beta / low risk exposure turned out to be the very opposite.

The scars from this episode still run deep.

But real estate is not always about low risk / low return. It is about generating a competitive total return so long as you can hold through cycle. Forced selling at moments of distress is the surest way to wealth destruction. To own real estate, one must be prepared both financially and emotionally to ride out the cycle.

The rewards for doing so can be significant.

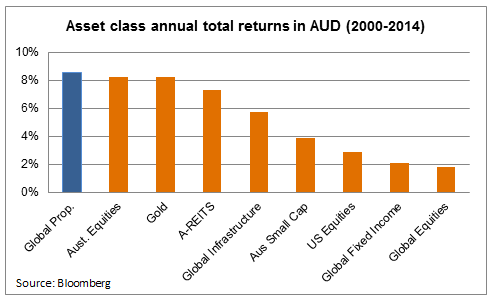

In the 15 years to 31 December 2014, listed global real estate (measured in AUD) has been one of the best performing asset classes. Listed domestic (Australian) real estate is not far behind.

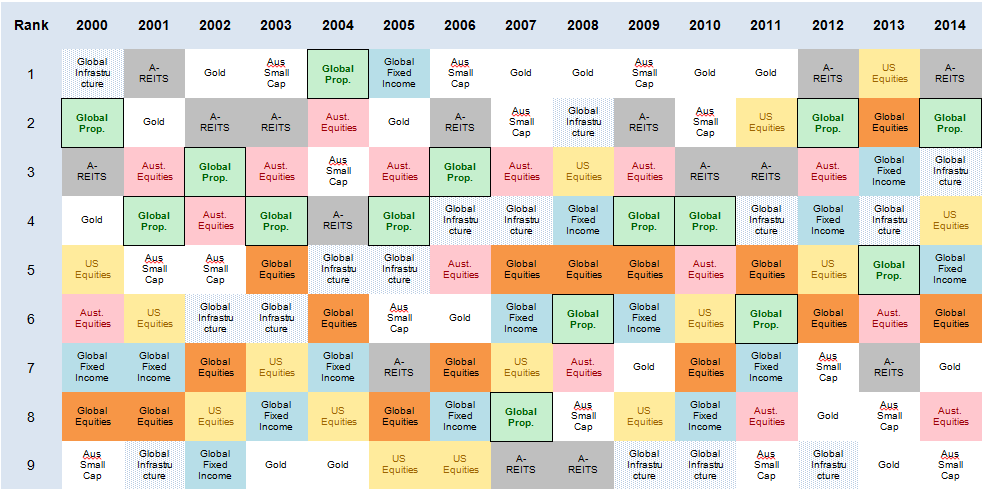

What is equally important is the relative consistency in return. The following table ranks sector performance by calendar year – global real estate (shown in green) is more often than not a better than average performer across assets classes.

Source: Credit Suisse

Of course, the traumatic events of 2007-2008 showed real estate to be vulnerable to significant credit events. This should be no surprise – since real estate is effectively a lending business. Access to capital is fundamental to its ownership, as any home owner would attest.

The lessons to be learnt from the table above and the 15 years of observed data are:

- over time, global real estate does generate competitive total returns;

- on a year to year basis, global real estate is a relatively consistent performer relative to other asset classes – highlighting the importance of yield in total return;

- however, to extract the best returns, one must be prepared to hold through the ‘dark times’. And there will always be dark times in real estate.

To be fair, we did not need 15 years of data to confirm these lessons. Wealthy US and European families who hold wealth in land have known this fact for hundreds of years.

Why global?

In a word - choice. While Australian listed real estate is significant in size, it provides very limited access to sectors expected to benefit from some of the strongest real estate themes. Listed real estate entities investing in health, aged care, student housing, and apartment (rental) sectors are very limited or non-existent in Australia.

With respect to aged care and health, it is worth highlighting over 10,000 Americans are turning 65 every day. Demand for aged care facilities, memory care and long-term health facilities is expected to increase significantly over the next five years – more so over 10 years.

Global real estate companies like Ventas, Cofinimmo, Omega and LTC properties are well placed, and of sufficient scale to benefit from this clear demographic trend. Importantly, these companies have very limited or no operational exposure to the risk associated with providing health services. The real estate entities or REIT businesses collect rent from the underlying operator, whose whole business is entirely dependant on the physical infrastructure these REITs provide.

In effect, Health Care REITs are the most senior capital providers to companies at the forefront of this demographic trend. They collect rent, minimise operational risk, and claim long-term upside with higher rents over time.

This is an attractive business model.

But apart from a handful of very small local REITs, access to this opportunity in Australia is limited.

Different but no less powerful investment themes are in place for student housing, residential rental accommodation, and self-storage. Sectors that are very small or non-existent in Australia listed real estate.

Why global? To access and benefit from the most important and powerful investment themes which are not readily available or of sufficient scale in Australia.

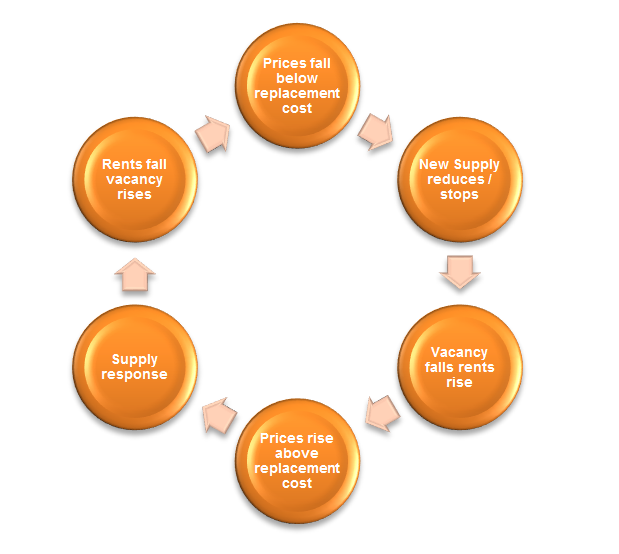

The real estate cycle

Normally, a real estate cycle can be characterised as per the following.

In reality, there can be significant lags between the price signal and the supply response due to financial and approval delays. This lag extends the cycle and can create ‘booms and busts’.

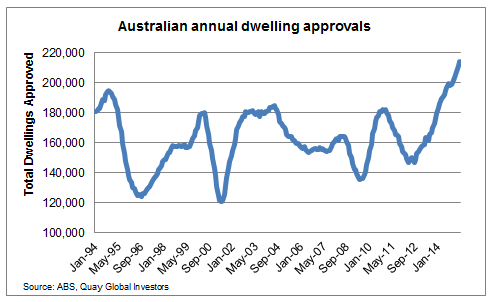

The hot topic today is Australian residential property. We will restrain ourselves from commenting whether Australia has a ‘property bubble’ but instead simply highlight the following chart – which clearly shows a very significant supply response to the recent rise in dwelling prices. Based on a normal real estate cycle, what comes next is fairly obvious.

The medium-term threat to real estate returns

Quite often, non real estate experts will often suggest rising interest rates spells doom for property investment. Most property experts know this is not the case. Consider the following:

- Real estate has been a very poor long-term performer in Japan – despite near zero interest rates for 20 years.

- After the real estate bubble burst in 1991, interest rates were reduced from 6% to 0.5% - after which land values fell a further 30%;

- the strongest residential cycle in Australia occurred in the late 1980s – when mortgage rates approach 17%;

- the rising US interest rate cycle from 2002 to 2007 was accompanied by a rise in listed and unlisted commercial real estate values,

- and the move to a 0.25% cash rate in 2008 did little to turn around the real estate market in 2009.

In our opinion, the main threat to real estate returns is supply. Supply creates competition for tenants, which in turn pushes rents down, resulting in falling values.

One of the most interesting dynamics in global real estate today is despite rising rents and prices, we have yet to see any meaningful supply response outside of Australia.

The current underlying fundamentals for global real estate are (generally) robust

What is sometimes not fully appreciated in Australia is how traumatic the financial crisis was in the Northern Hemisphere. Australia was somewhat fortunate to miss the worst of the knock-on effects of rising unemployment, economic contraction and widespread bank insolvency.

The legacy of the financial crisis was a significant reduction in risk appetite across the global banking industry. Real estate lending was not a great area for career advancement for bankers after 2009 and access to capital for developers and owners became very difficult.

In 2010 and 2011, lending improved for established (well leased) assets, but lending for risk assets (brownfield and greenfield developments) was still hard to obtain. Moreover, the near death experience suffered by senior real estate executives and boards kept the real estate industry very risk averse.

The outcome has been a minimal or almost no supply response.

US residential

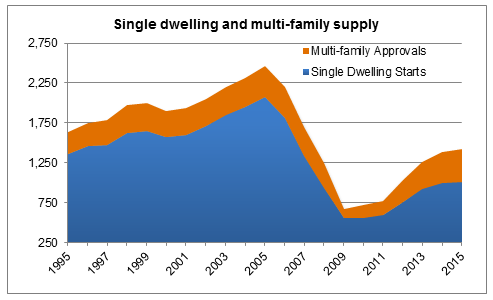

The strong performance of multi-family asset prices has triggered a strong supply response in the sector. Current unit approvals are running at 400k per annum versus long-term average of 308k.

However, when viewed in the context of total housing (including single family structure), supply is barely back to trend after several years below. The result has been very strong rental growth – especially in the West Coast where planning restrictions are more robust, compared to the East.

It is hard to see single housing return to prior peaks given the on-going reluctance for banks to return to the mortgage business in the same manner as the early 2000s. Credit scores have been tarnished, and student loans per person are at all time highs – surely delaying the purchase of the first home.

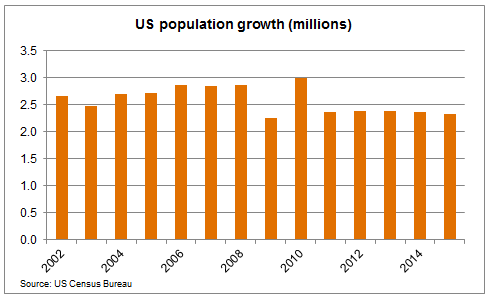

This decline in new housing supply is set against the backdrop of on- going population (and household formation) growth.

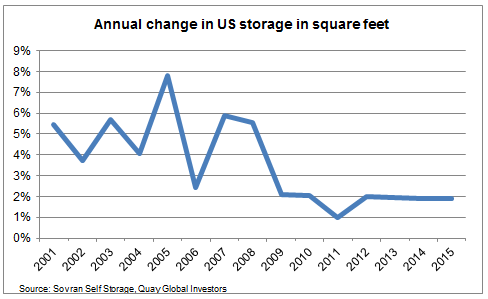

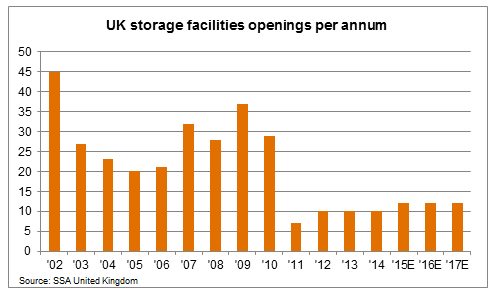

Self-Storage

Self-storage is an extremely difficult asset class to accumulate on an institutional scale as assets can have a unit value as low as $5m. Historically, supply comes from local developers who best understand local planning restrictions and for whom a margin on $5m is meaningful.

Lack of available funding for local developers has had a negative impact on new supply in the US and UK.

The result is a highly fragmented industry but one where some select listed real estate groups are building scale and generating attractive shareholder returns in the process.

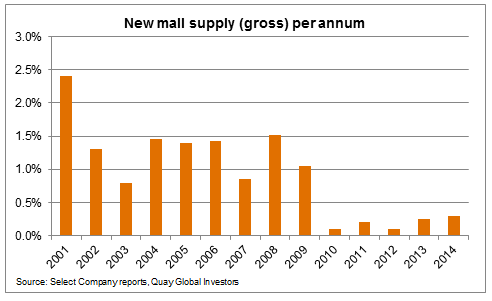

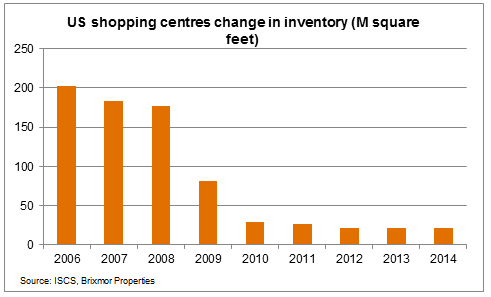

Retail

The Retail sector has had two constraints – funding and the risk of online retail. The result has been a collapse in new supply for both malls…

…and grocery-based shopping centres.

While the threat of the online on retail is real, we believe most retailers will always require or desire a bricks and mortar address, even if a loss leader for their e-commerce strategy. It makes sense that retailers will seek to locate these stores in the centres with the highest number of visitors – i.e. the most productive or ‘fortress’ malls.

At the other end of the scale, people like convenience and freshness when it comes to groceries and everyday items; to date, online hasn’t been able to successfully execute this.

Within retail, we believe there are favourable fundamentals for these two types of retail assets, particularly when considered in light of the lack of recent supply.

We believe those most exposed to the online threat are the mid-market retailers and the assets they are located in - centres generally anchored by discount department stores in peripheral locations.

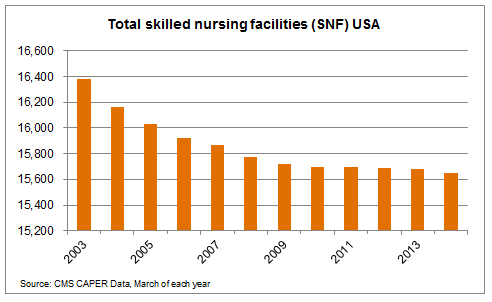

Health Care

Despite the clear need to cater for an aging population and increase in long-term medical issues such as memory care, the provision of skilled nursing facilities has declined over the past 10 years (while the number of beds has remained static).

Concluding thoughts

Why global real estate?

- Real estate (land) is the oldest form of investment, and for generations has proven to be a reliable store of wealth.

- Through cycle, global real estate has delivered very competitive total returns in AUD terms.

- During the past 15 years, global real estate has consistently performed well on a per calendar year basis. Never being the worst performer, and being one of the top two asset classes on four occasions (versus Australian Equities which was the top performer once).

- Global real estate allows investors to benefit from listed asset classes not easily accessible in Australia (Health, Student Housing, Self-Storage, Residential and Rental).

- The fundamentals for select real estate markets are extremely robust. Restricted funding has limited supply and with improving demand, strong rental growth has emerged. A trend likely to continue in many markets and sectors.

In our opinion, these attributes make listed global real estate complementary to any diversified investment strategy.

Disclaimer

The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. In particular this newsletter is not directed for investment purposes at US persons.